Editorial Disclaimer: This article is for general educational purposes only. Claimifio is not a licensed insurance agent or financial advisor. Always consult a licensed professional before making any insurance or financial decisions.

Beyond the App: Why Your Personal Policy Isn’t Enough for Uber & Lyft

You’ve got your car, your smartphone, and the open road. As an Uber or Lyft driver in the USA, you’re part of a dynamic gig economy, enjoying flexibility and earning potential. But there’s a critical area many drivers overlook, often at their peril: car insurance for Uber & Lyft in the USA.

It’s a common misconception that your standard personal auto insurance policy fully covers you while driving for a rideshare company. The truth is, it usually doesn’t. In fact, relying solely on a personal policy while driving for a rideshare app can lead to devastating out-of-pocket expenses and claim denials. This critical gap in coverage can put your vehicle, your finances, and your livelihood at severe risk.

This handbook will demystify car insurance for Uber & Lyft in the USA, guiding you through the unique insurance landscape. We’ll break down the infamous “coverage gap,” explain the insurance provided by Uber and Lyft, and reveal the best strategies and policy options to ensure you’re fully protected from the moment you log on until you drop off your last passenger.

1. The Critical “Coverage Gap”: Why Rideshare Insurance is Essential

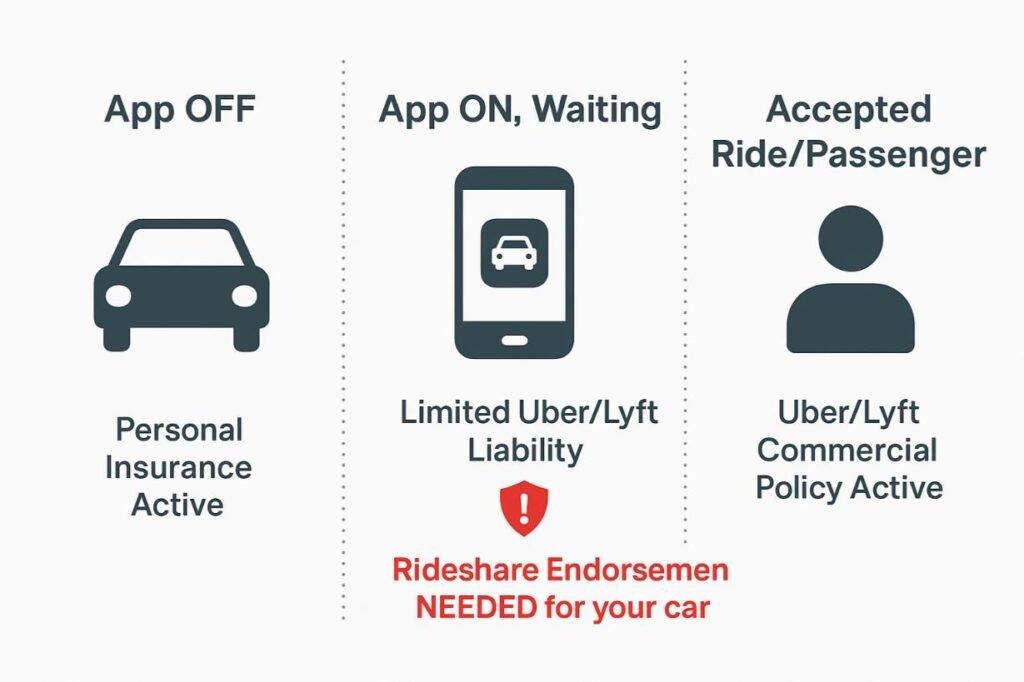

The biggest challenge for rideshare drivers is understanding the “coverage gap” that exists between your personal auto insurance policy and the commercial policies provided by Uber and Lyft.

Your Personal Auto Policy:

- During Personal Use (Off-App): Fully active.

- During Rideshare Use: Most personal auto policies exclude coverage for any “for-hire” or commercial activity. If you get into an accident while logged into the app, your personal insurer will likely deny the claim, leaving you completely exposed.

Uber & Lyft’s Commercial Policies:

Uber and Lyft do provide commercial insurance for their drivers, but this coverage is tiered and changes depending on which “period” of rideshare activity you are in.

- Period 0 (App Off): You’re just driving your car for personal use. Your personal auto policy is active.

- Period 1 (App On, Waiting for a Request): You’re logged into the app and available to accept a ride. Uber/Lyft’s limited liability coverage is active (typically $50,000 Bodily Injury per person/$100,000 per accident and $25,000 Property Damage). Crucially, their comprehensive and collision coverage is NOT active here, leaving your vehicle unprotected if you’re at fault.

- Period 2 (Accepted Request, Driving to Pick Up Passenger): You’ve accepted a ride and are on your way to the pickup location. Uber/Lyft’s full commercial insurance is active (typically $1,000,000 third-party liability, plus contingent comprehensive and collision with a high deductible).

- Period 3 (Passenger in Car, Driving to Destination): The passenger is in your vehicle. Uber/Lyft’s full commercial insurance is active (same as Period 2).

The Rideshare “Coverage Gap”:

The most significant gap exists in Period 1. While Uber/Lyft offer limited liability, your personal comprehensive and collision coverage is inactive, and Uber/Lyft’s doesn’t kick in yet. If you cause an accident while waiting for a ride request, your personal insurer will deny your claim (because you were driving commercially), and Uber/Lyft won’t cover your vehicle damage (because you didn’t have a passenger or an accepted ride). This is why specific rideshare insurance is so vital.

2. Your Best Options: Car Insurance for Uber & Lyft in the USA

To adequately protect yourself and your vehicle, you need to bridge the “coverage gap.” Here are the primary solutions for Uber driver insurance and Lyft driver insurance:

A. Rideshare Endorsement (The Most Common & Recommended)

- What it is: This is an add-on (or “endorsement”) to your existing personal auto insurance policy. It extends your personal coverage to include the time you spend in Period 1 (app on, waiting for a request).

- Benefits: It effectively closes the “coverage gap,” ensuring your vehicle is covered by your own collision and comprehensive coverage (with your chosen deductibles) during this vulnerable period. It also smooths the transition between personal and rideshare coverage, reducing potential headaches during a claim.

- Cost: Relatively affordable, often adding 10-25% to your personal premium.

- Availability: Many major insurers now offer this (e.g., GEICO, Progressive, State Farm, Allstate, Farmers, USAA, Liberty Mutual, Travelers, Safeco). Availability varies by state and insurer.

B. Hybrid Personal/Commercial Policy

- What it is: Some insurers offer specific policies designed entirely for rideshare drivers, blending personal and commercial coverage into one product.

- Benefits: Comprehensive coverage designed specifically for your unique needs.

- Cost: Can be more expensive than a simple endorsement, but might be more comprehensive depending on the provider.

- Availability: Less common than endorsements, but growing.

C. Commercial Auto Insurance (Usually Not Necessary for Most)

- What it is: A full-fledged commercial auto policy.

- Benefits: Provides the most robust coverage for all periods of rideshare driving and generally has higher limits.

- Cost: Significantly more expensive than personal auto with an endorsement.

- When it might be needed: If you exclusively drive for rideshare full-time, put an extreme number of miles on your vehicle, or are mandated by certain local regulations. For most part-time drivers, it’s overkill and too costly.

Understanding how different coverages work, like Collision and Comprehensive, is crucial for rideshare drivers. Dive deeper with our Ultimate Guide: Understanding Full Coverage Car Insurance in the USA.

Key Considerations When Choosing Rideshare Insurance

When selecting the best rideshare insurance for your needs, keep these points in mind:

- Company vs. Endorsement: Does your current personal insurer offer a rideshare endorsement? If not, you’ll need to find one that does or switch providers.

- Deductibles: Uber and Lyft’s contingent comprehensive and collision coverage often comes with a high deductible (e.g., $1,000 or $2,500). Ensure you’re comfortable paying this if you rely on their coverage in Periods 2/3. Your rideshare endorsement might allow you to use your lower personal policy deductible in Period 1.

- UM/UIM Coverage: Uber/Lyft’s policies might not always include Uninsured/Underinsured Motorist coverage during all periods. Check if your state requires it, and ensure your personal policy with the endorsement extends this protection.

- Medical Payments/PIP: Confirm how your MedPay or PIP coverage works during rideshare activities.

- Gap Insurance: If you have a car loan or lease, check how the rideshare endorsement affects your gap insurance, as traditional gap policies may not cover commercial losses.

Hypothetical Scenario A: The Period 1 Accident

Jessica, an Uber driver in Chicago, is logged into the Uber app and waiting for a ride request. While stopped at a red light, another driver runs a stop sign and T-bones her car. The other driver is at fault but has minimal liability insurance.

- Without Rideshare Endorsement: Jessica’s personal auto insurer would deny her claim for her own vehicle damage because she was “for-hire.” Uber’s commercial comprehensive/collision wouldn’t kick in because she hadn’t accepted a ride. She would be completely out-of-pocket for her car’s repairs.

- With Rideshare Endorsement: Her personal collision coverage (extended by the endorsement) would pay for her car’s damage, minus her personal deductible. Her Uninsured Motorist coverage (if she has it and it extends to rideshare) would help cover additional damages not covered by the at-fault driver’s minimal policy.

4. How to Get the Best Car Insurance for Uber & Lyft

Finding the right rideshare insurance doesn’t have to be complicated:

- Contact Your Current Insurer First: Ask if they offer a rideshare endorsement. If so, get a quote to add it to your policy. This is often the easiest and most affordable option.

- Shop Around: If your current insurer doesn’t offer a rideshare endorsement or the price is too high, get quotes from other major providers known for rideshare-friendly policies (e.g., GEICO, Progressive, State Farm, Allstate).

- Be Transparent: Always be honest with insurance companies about your rideshare activities. Failing to disclose it can lead to claim denials.

- Review Uber/Lyft’s Current Policies: Insurance details can change. Regularly check the insurance sections on the Uber and Lyft driver portals for the most up-to-date information on their provided commercial coverage.

Hypothetical Scenario B: Max’s Full-Time Gig

Max drives for Lyft full-time in Los Angeles, putting 40+ hours a week and over 30,000 miles a year on his car. He wants ironclad protection.

- Max’s Strategy: He compared several insurers. While a rideshare endorsement was available, he found a specialized hybrid personal/commercial policy from an insurer that caters specifically to full-time gig drivers. This policy offered slightly higher liability limits and a lower comprehensive/collision deductible that applied consistently across all periods of his driving, giving him greater peace of mind for his livelihood.

- Why it works: For Max’s high-usage scenario, the slightly higher cost of the hybrid policy was justified by the superior and seamless protection it offered, making it the best car insurance for gig workers like him.

For the most up-to-date and authoritative information on Uber’s insurance policies for drivers, always refer directly to Uber’s official website.

FAQ: Car Insurance for Uber & Lyft

Q: Do I need rideshare insurance if Uber/Lyft provide coverage?

A: Yes. Their coverage is specifically designed to protect them and your passengers, with significant gaps in coverage for your vehicle, especially in Period 1 (app on, waiting for a request). A rideshare endorsement closes this gap.

Q: What happens if I don’t tell my personal insurer I drive for Uber/Lyft?

A: If you get into an accident while logged into the app, your personal insurer will likely deny your claim because you violated the terms of your policy (driving for “for-hire” purposes). This could lead to massive out-of-pocket costs.

Q: Is rideshare insurance expensive?

A: A rideshare endorsement (add-on to your personal policy) is generally quite affordable, often adding 10-25% to your personal premium. It’s a small price to pay for significant protection.

Q: Does rideshare insurance cover me for personal use of my car?

A: Yes, a rideshare endorsement works by extending your personal policy. When your app is off, your personal auto insurance (with the endorsement) covers you just as it normally would for personal use.

Q: What is the deductible like for rideshare claims?

A: If you rely on Uber/Lyft’s commercial coverage (Periods 2 & 3), their deductibles can be high (e.g., $1,000 or $2,500). If you have a rideshare endorsement, your personal policy’s lower deductible might apply for Period 1.

Drive Confidently: Secure Your Gig Economy Journey

The flexibility and earnings potential of being an Uber or Lyft driver in the USA are undeniable. But to truly thrive in the gig economy, you must safeguard your biggest asset: your vehicle, and your financial well-being. Understanding the nuances of car insurance for Uber & Lyft in the USA is not just smart, it’s essential.

Don’t let the “coverage gap” put you at risk. By investing in an affordable rideshare endorsement or a specialized hybrid policy, you ensure that every mile you drive, whether for a passenger or for personal use, is protected. Drive confidently, knowing your livelihood is secure.

Protect your investment and your income! Get a free, personalized quote for rideshare insurance today and bridge the coverage gap for your Uber or Lyft driving!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan is the founder of Claimifio, an independent insurance education publication helping everyday renters, homeowners, and expats understand their coverage rights and claims processes. With a background spanning 8+ years in digital publishing and content research, Imran has spent the last several years studying insurance policy language, policyholder rights, and the gaps between what people think their policy covers — and what it actually pays out. Every guide on Claimifio is researched from primary sources including the Insurance Information Institute, NAIC, and official policy documentation, and written in plain English so you can take action with confidence. Claimifio is an independent educational resource. We are not a licensed insurance agent, broker, or financial advisor. Always consult a licensed professional for advice specific to your situation.

Important Disclaimer: The content on Claimifio.com is for general educational and informational purposes only. We are not licensed insurance agents, brokers, or financial advisors. Nothing here constitutes professional insurance or financial advice. Insurance laws, rates, and requirements vary by state and country. Always consult a licensed insurance professional before making any policy decisions.