Editorial Disclaimer: This article is for general educational purposes only. Claimifio is not a licensed insurance agent or financial advisor. Always consult a licensed professional before making any insurance or financial decisions.

The Balancing Act: Your Car Insurance Deductible Explained

The car insurance deductible is perhaps the most misunderstood yet most financially significant term in your auto policy. It is the core financial lever that determines both your monthly premium and your out-of-pocket costs after an accident. Getting the deductible right is a crucial decision that helps you save money on your policy and manage risk effectively.

So, what is a car insurance deductible?

Simply put, the deductible is the amount of money you agree to pay out-of-pocket for covered repairs or losses before your insurance company steps in and pays the rest.

This ultimate guide will break down exactly how deductibles work, show you how they affect your premiums, and provide a comprehensive strategy for choosing a car insurance deductible that perfectly fits your financial situation and risk tolerance.

1. How Deductibles Work: The Financial Basics

The purpose of a deductible is twofold: to share the risk between you and the insurer, and to deter you from filing frivolous, small claims.

The Formula:

If you file a claim for covered damages, the payout works like this:

$$\text{Insurance Payout} = \text{Total Covered Damage Cost} – \text{Your Deductible Amount}$$

Example Scenario:

- You have a $500 deductible.

- Your vehicle sustains $3,000 in covered damage after a collision.

- You pay the repair shop $500 (your deductible).

- Your insurance company pays the repair shop **$2,500** ($3,000 – $500).

Key Facts About Deductibles:

- Per-Claim Basis: Unlike health insurance, where a deductible may be annual, car insurance deductibles apply per claim (or per covered incident). If you file three claims in one year, you must pay the deductible three times.

- Applies to Specific Coverages: Deductibles typically only apply to physical damage coverages, where you are claiming money for your vehicle:

- Collision Coverage (damage from impact with another object/car).

- Comprehensive Coverage (damage from fire, theft, hail, hitting an animal, etc.).

- Does NOT Apply to Liability: There is no deductible for Liability coverage, which pays for damage or injury you cause to others.

2. The Great Trade-Off: High vs. Low Deductible Car Insurance

When choosing a car insurance deductible, you are essentially deciding how much financial risk you are willing to take on personally versus how much you want your insurer to absorb. This decision creates an inverse relationship between your deductible and your premium:

A. High Deductible Car Insurance (e.g., $1,000, $1,500, $2,500)

| PROS (Savings) | CONS (Risk) |

| Significantly Lower Premiums | Higher immediate out-of-pocket cost if you file a claim. |

| Maximum Premium Savings over time if you rarely file claims. | May deter you from filing smaller, legitimate claims. |

| Less likely to have your rates increase due to a small claim. | Potential financial strain if you lack the emergency funds to cover the deductible. |

| Good for safe drivers with emergency savings. |

B. Low Deductible Car Insurance (e.g., $100, $250, $500)

| PROS (Security) | CONS (Cost) |

| Lower Out-of-Pocket Cost after an accident. | Significantly Higher Premiums and overall annual cost. |

| Reduced Financial Stress after a major accident. | Reduced long-term savings compared to a high deductible. |

| Covers more smaller claims where the damage is just above the deductible amount. | You may lose the premium savings advantage if you file too many small claims. |

| Good for drivers with limited savings or high-risk profiles. |

Analogy: Think of the deductible as your self-insurance amount. If you are financially capable of “self-insuring” the first $1,000 or $2,000 of damage, you get rewarded with lower monthly payments.

3. The Smart Strategy: Choosing a Car Insurance Deductible

The most common deductible amounts in the US are $500 and $1,000. To choose the right one, follow these three steps:

Step 1: Assess Your Financial Readiness (The Emergency Fund Test)

Ask yourself: Can I comfortably write a check for the deductible amount TODAY without dipping into funds needed for rent or groceries?

- If YES: You can afford a higher deductible, potentially $1,000 or more. You have the freedom to accept more risk in exchange for maximum premium savings.

- If NO: You must choose a lower deductible, such as $500 or $250. Paying a slightly higher monthly premium is a safer financial choice than facing a bill you cannot afford after an accident.

Step 2: Evaluate Your Driving Risk and Vehicle Value

- High-Risk Drivers: (New drivers, long commutes, poor driving record, driving in high-traffic urban areas)

- Recommendation: Consider a lower deductible ($500). Since you are statistically more likely to file a claim, paying a slightly higher premium guarantees manageable out-of-pocket costs when the accident occurs.

- If you fall into this category, understanding the full post-accident process is key: What Happens After a Car Accident: Your Step-by-Step Insurance Guide.

- Low-Risk Drivers: (Experienced drivers, clean record, low annual mileage)

- Recommendation: Consider a higher deductible ($1,000+). Your low probability of filing a claim makes maximizing premium savings over time a smart bet.

- Low-Value Vehicles: (Older cars, Actual Cash Value (ACV) under $5,000)

- Recommendation: Opt for the highest deductible possible (e.g., $1,500 or $2,000). The potential insurance payout (ACV minus deductible) might be so low that paying for Collision/Comprehensive coverage isn’t even worth the premium.

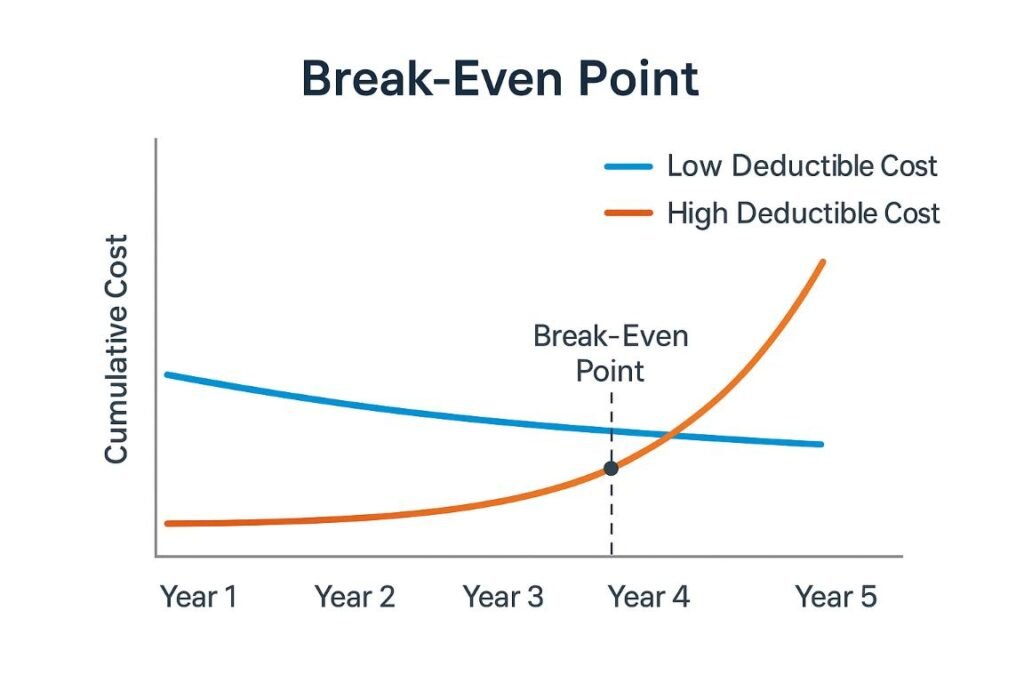

Step 3: Calculate the Break-Even Point

Always calculate the premium savings associated with raising your deductible.

Scenario Comparison:

- Option A: $500 Deductible = $1,500 annual premium.

- Option B: $1,000 Deductible = $1,200 annual premium.

By choosing Option B, you save **$300 per year** ($1,500 – $1,200).

- Break-Even Point: The extra risk you took on is $500 ($1,000 – $500).

- Time to Break-Even: You need to go $500 / $300 = 1.67 years without filing a claim to break even. If you remain accident-free for longer than that, you are saving money. If you have an accident before that time, you “lose” the premium savings.

Pro Tip: Ask your agent to run quotes for deductibles at $500, $1,000, and $2,000. You may find that the premium drops significantly when moving from $500 to $1,000, but only marginally when moving from $1,000 to $2,000. Find the insurer’s “sweet spot” where the premium reduction is maximized.

4. Deductibles in Specialized Coverages

While Collision and Comprehensive are the main areas for deductibles, they can also apply to other specialized types of coverage:

- Glass Coverage: Some insurers offer a separate, low or even $0 deductible option for glass-only claims (like a chipped windshield). This is often worthwhile if you live in an area with high road debris.

- Uninsured/Underinsured Motorist Property Damage (UMPD): In some states, UMPD coverage (which pays for your car damage if an uninsured driver hits you) may have a deductible, though it is often lower than your standard Collision deductible.

5. When the Deductible Doesn’t Apply

It is important to know when you do not have to pay a deductible:

- If You Are Not At Fault: If another driver is deemed 100% at fault for the accident, their Liability coverage pays for your damages. You may pay your deductible upfront to speed up repairs (filing through your Collision coverage), but your insurance company will usually subrogate (get the money back) from the at-fault driver’s insurer and reimburse your deductible.

- Liability Claims: As mentioned, your deductible only applies to claims for your vehicle. Liability claims for damage or injury you cause to others do not involve a deductible.

- Medical Payments/PIP: Medical Payments and Personal Injury Protection (PIP) coverages typically do not have a deductible.

Drive Smart, Insure Smarter

Your deductible is more than just a number on a policy; it’s a strategic financial choice that dictates your budget and your risk profile. While low deductible car insurance buys you peace of mind with higher monthly payments, high deductible car insurance rewards disciplined, safe drivers with immediate premium savings.

By using the three-step strategy—assessing your emergency funds, analyzing your risk, and calculating the break-even point—you can stop guessing and confidently select the deductible that is best for your wallet and your security.

Ready to take control of your premiums? Contact your insurance provider today and ask them for quotes based on a $500, $1,000, and $2,000 deductible to find your optimal savings point!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan is the founder of Claimifio, an independent insurance education publication helping everyday renters, homeowners, and expats understand their coverage rights and claims processes. With a background spanning 8+ years in digital publishing and content research, Imran has spent the last several years studying insurance policy language, policyholder rights, and the gaps between what people think their policy covers — and what it actually pays out. Every guide on Claimifio is researched from primary sources including the Insurance Information Institute, NAIC, and official policy documentation, and written in plain English so you can take action with confidence. Claimifio is an independent educational resource. We are not a licensed insurance agent, broker, or financial advisor. Always consult a licensed professional for advice specific to your situation.

Important Disclaimer: The content on Claimifio.com is for general educational and informational purposes only. We are not licensed insurance agents, brokers, or financial advisors. Nothing here constitutes professional insurance or financial advice. Insurance laws, rates, and requirements vary by state and country. Always consult a licensed insurance professional before making any policy decisions.