Editorial Disclaimer: This article is for general educational purposes only. Claimifio is not a licensed insurance agent or financial advisor. Always consult a licensed professional before making any insurance or financial decisions.

| ⚡ QUICK ANSWER — How Do You File a Health Insurance Claim? |

| To file a health insurance claim: (1) Receive medical care from an in-network provider — they usually file the claim automatically on your behalf. (2) If you used an out-of-network provider or paid out of pocket, download a claim form from your insurer’s website, attach your itemized medical bill, and submit by mail, fax, or online portal. (3) Wait 30–60 days for processing. (4) Review your Explanation of Benefits (EOB) to confirm what was paid. (5) Pay any remaining balance owed. If denied, you have the right to appeal. |

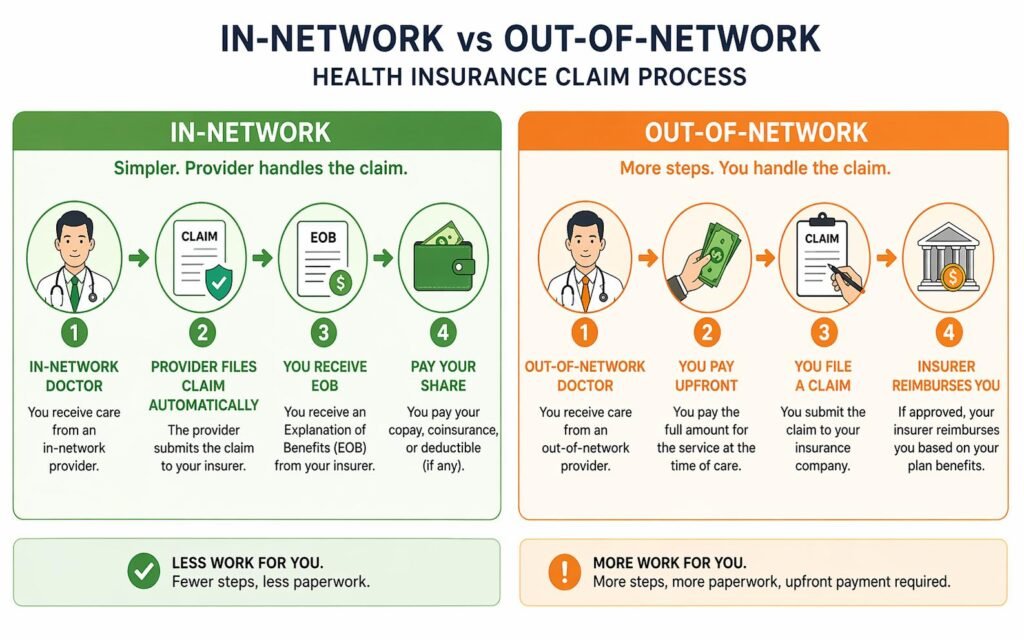

1. Do You Actually Need to File a Claim? (Most People Don’t)

Here is the most important thing most people don’t realize about health insurance claims: if you visit an in-network doctor, hospital, or lab — they file the claim for you automatically. You do nothing except show your insurance card at check-in.

The claims process only becomes your responsibility in these specific situations:

- You used an out-of-network provider and paid the bill yourself upfront.

- You paid out of pocket (for any reason) and want reimbursement from your insurer.

- Your provider forgot to bill your insurance and sent the bill directly to you.

- You received care abroad while traveling and need international reimbursement.

- You purchased a medical device, equipment, or prescription and need reimbursement.

| 💡 Key Insight |

| About 85–90% of health insurance claims in the USA are filed directly by the provider — not the patient. |

| Your job in most cases is simply: show your insurance card, receive care, wait for the EOB, then pay your share (copay/coinsurance) to the provider. |

| This guide covers the cases where YOU need to take action. |

2. Before You Get Medical Care — What to Check First

The best way to avoid claim problems is to take these steps BEFORE your medical appointment — not after.

- Verify your provider is in-network Call your insurer (number on the back of your card) or check their online provider directory. Search by the provider’s name AND their NPI (National Provider Identifier) number if possible — doctors can be in-network at one location but out-of-network at another. Ask the provider’s office directly: ‘Do you accept [Insurance Name] insurance?’ — always double-check even if the online directory says yes.

- Check if prior authorization is required Certain procedures, specialist visits, imaging (MRI, CT scans), and medications require pre-approval from your insurer before you receive them. Ask your doctor: ‘Does this require prior authorization from my insurance?’ If required and not obtained — your claim can be denied even if the service was medically necessary.

- Bring your insurance card to every appointment Your insurance card contains your Member ID, Group Number, and insurer contact information — all required for the provider to file your claim. If you don’t have a physical card, most insurers have mobile apps where you can access a digital card. Without your card details, providers may bill you directly instead of your insurer.

- Save all receipts and itemized bills Request an itemized bill (not just a summary) from every provider — this lists each service, its billing code, and individual cost. You will need this if you file your own claim or if you need to dispute a billing error. Store digitally — photograph or scan every bill immediately.

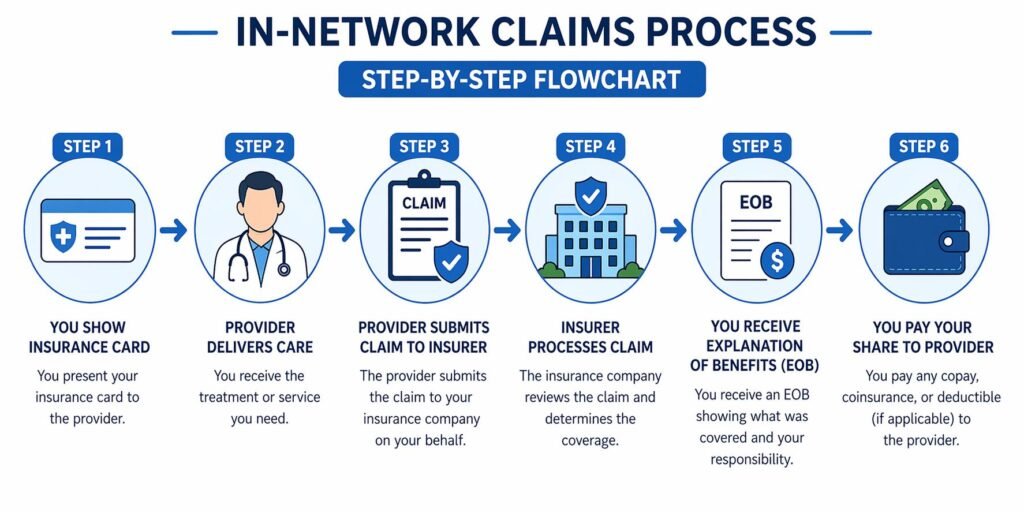

3. Step-by-Step: Filing an In-Network Claim

When you use an in-network provider, the claims process is almost entirely handled for you. Here is exactly what happens:

- Show your insurance card at check-in. The provider’s billing department uses your Member ID and Group Number to verify your coverage and file the claim.

- Receive your medical care. The provider delivers the service. Pay your copay at this point if your plan requires it.

- Provider submits the claim to your insurer. The provider sends an electronic claim (called a CMS-1500 form for outpatient or UB-04 for hospital) directly to your insurance company — usually within a few days of your visit.

- Insurer processes the claim. Your insurance company reviews the claim, applies your deductible if not yet met, calculates your coinsurance, and determines what they will pay. This takes 14–30 days for standard claims.

- You receive an Explanation of Benefits (EOB). Your insurer sends you an EOB by mail or through your online account. This is NOT a bill — it is a summary of what was billed, what your insurer paid, and what you owe. Review it carefully.

- Provider sends you a bill for your share. After receiving payment from your insurer, the provider bills you for the remaining balance (your deductible portion, copay if not paid, coinsurance). Compare this bill to your EOB before paying.

| ⚠️ Never Pay a Medical Bill Before Receiving Your EOB |

| Many providers send bills before your insurance has processed the claim. Do not pay immediately. |

| Wait for your EOB, compare what the provider is billing you against what your EOB says you owe. |

| Billing errors affect approximately 80% of medical bills in the USA — always verify before paying. |

4. Step-by-Step: Filing an Out-of-Network or Reimbursement Claim

If you paid for care out of pocket, used an out-of-network provider, or received care abroad, you need to file the claim yourself to get reimbursed. Here is the exact process:

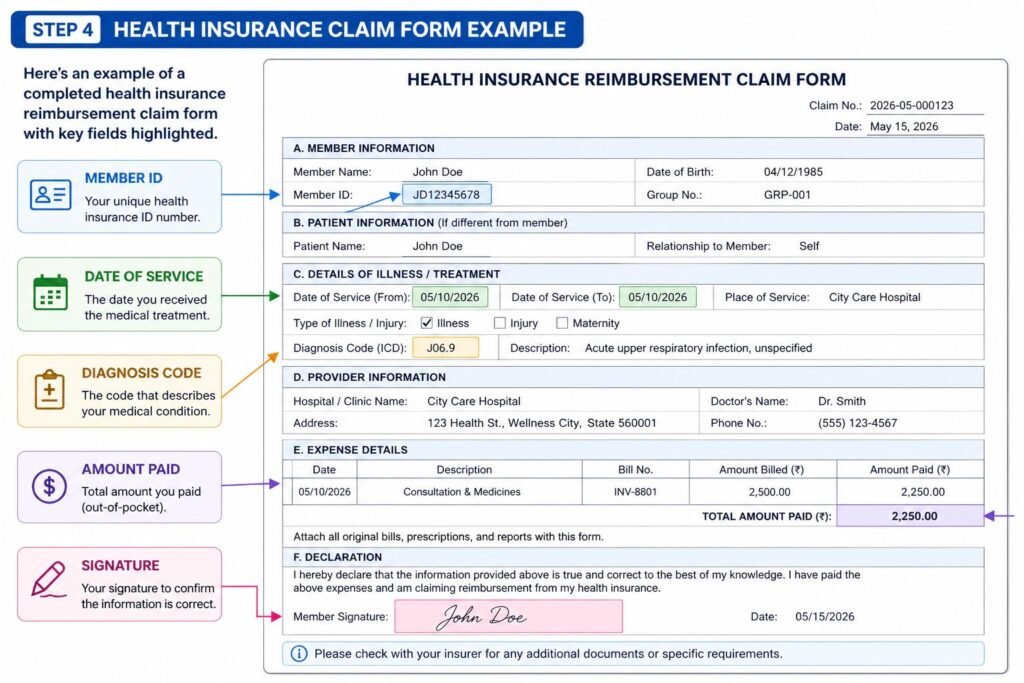

- Get an itemized bill from your provider Request a detailed itemized bill — not a summary statement. It must include: provider’s name and NPI, date of service, diagnosis code (ICD-10), procedure codes (CPT codes), and cost per service. Without these specific details, your insurer will reject the claim immediately.

- Download your insurer’s claim form Log into your insurer’s website or mobile app and find the ‘Claims’ or ‘Reimbursement’ section. Download their standard claim form — most insurers call this a ‘Medical Claim Form’ or ‘Member Reimbursement Form’. Common insurers and their claim portals: UnitedHealthcare (myuhc.com), Aetna (aetna.com), Cigna (mycigna.com), Blue Cross (bcbs.com).

- Complete the claim form Fill in: your name, member ID, date of birth, provider details, date of service, diagnosis, and the amount paid. Be precise — even small errors (wrong date, wrong member ID digit) cause rejections. Sign and date the form — unsigned forms are automatically rejected.

- Attach all supporting documents Attach your itemized bill, proof of payment (receipt or bank statement), and any referral or prior authorization documents if applicable. For overseas claims: also attach proof of travel (boarding passes, hotel receipts) and foreign currency conversion documentation. Make copies of everything before submitting — keep originals.

- Submit your claim Submit by: online portal (fastest), email/fax (medium), or mail (slowest — use certified mail and keep tracking number). Note your submission date and take a screenshot or get confirmation. Most insurers have a claims filing deadline — typically 90 days to 1 year from date of service. Do NOT delay.

- Track and follow up Most insurers allow claim status tracking online or via app. Standard processing time: 30–45 days. If no response after 45 days, call your insurer’s claims department. Always note the date, time, representative’s name, and reference number for every phone call.

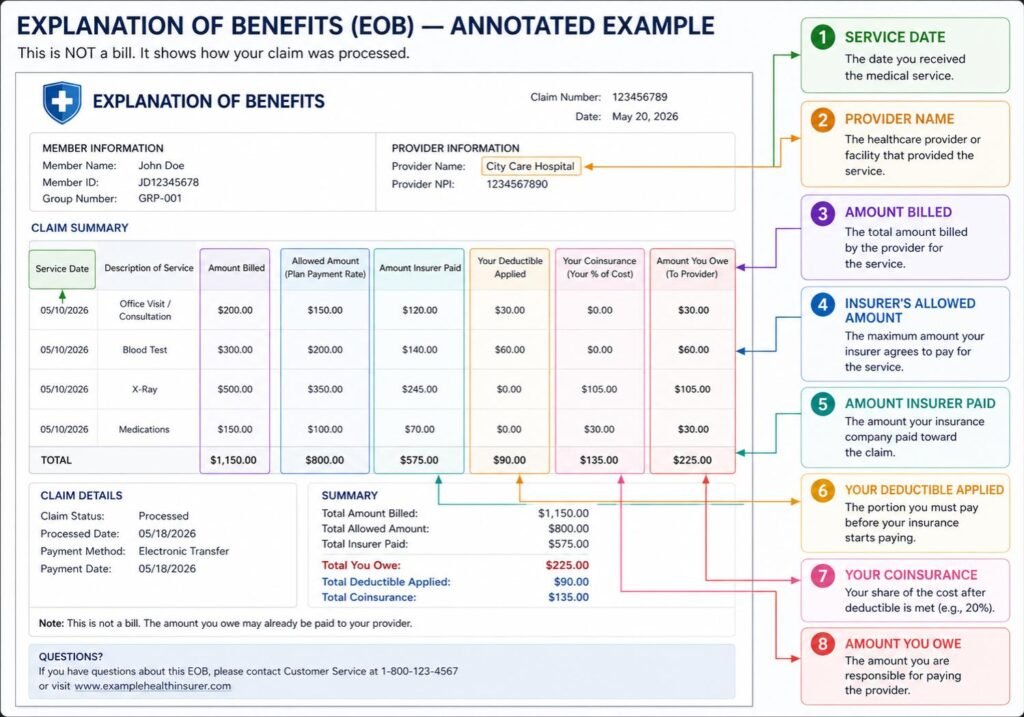

5. How to Read Your Explanation of Benefits (EOB)

Your EOB is not a bill — it is a summary statement your insurer sends after processing a claim. Understanding it is essential to verifying you’re being charged correctly.

| EOB Field | What It Means | What to Check |

| Amount Billed | What your provider charged | Should match your itemized bill exactly |

| Allowed Amount | Maximum your insurer will pay for this service | If lower than billed, the difference is ‘adjusted off’ — you don’t owe it (in-network) |

| Plan Paid | What your insurance actually paid | Verify this matches your expected coverage |

| Deductible Applied | How much counted toward your annual deductible | Track this to know when your deductible is fully met |

| Copay/Coinsurance | Your share of the allowed amount | This is what you will owe the provider |

| Member Responsibility | Total amount you owe after insurance | This should match what the provider bills you |

| Claim Status | Approved / Denied / Pending | If denied — note the denial reason code for your appeal |

6. Why Claims Get Denied — and How to Avoid It

Claim denials are extremely common — and most are preventable. Here are the most frequent reasons insurers deny health insurance claims:

| Denial Reason | How to Prevent It |

| Out-of-network provider used | Always verify in-network status before appointments |

| Prior authorization not obtained | Ask your doctor before every procedure if pre-auth is needed |

| Service deemed not medically necessary | Ensure your doctor documents medical necessity clearly in your records |

| Billing code error by provider | Ask for itemized bill and review CPT/diagnosis codes for accuracy |

| Claim filed after deadline | File within 90 days of service — never delay |

| Duplicate claim submitted | Track submitted claims — don’t resubmit without contacting insurer first |

| Member not eligible on date of service | Verify your coverage is active before each appointment |

| Missing or incorrect information | Double-check Member ID, date of birth, and all form fields before submitting |

| Referral not obtained (HMO) | Always get a written referral from your PCP before seeing a specialist |

| Experimental or excluded service | Check your plan’s exclusions list before scheduling non-standard treatments |

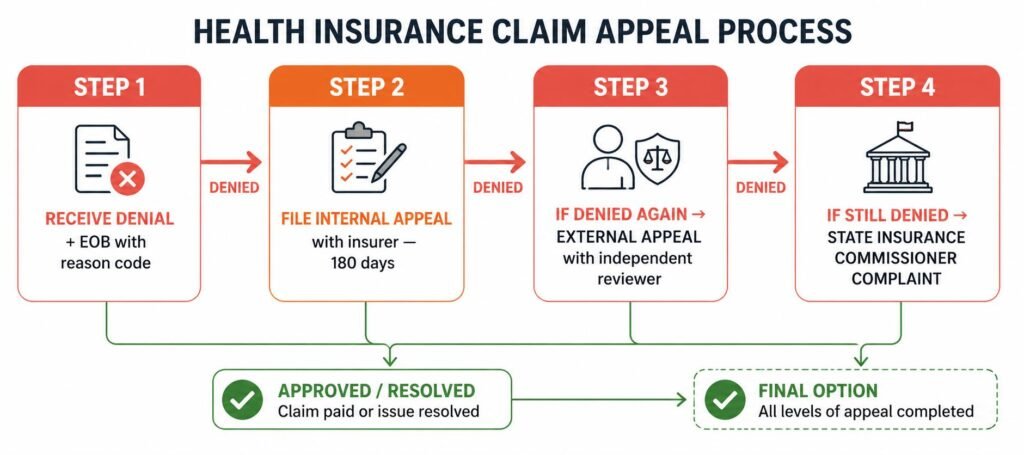

7. How to Appeal a Denied Health Insurance Claim

A denial is not final. You have a legal right to appeal under the ACA, and approximately 40% of appealed claims are ultimately overturned. Here is the process:

- Read your denial letter carefully. Your insurer must provide a written denial with a specific reason code and explanation. The reason code tells you exactly what to address in your appeal.

- Gather supporting documentation. Collect: your doctor’s notes supporting medical necessity, relevant medical records, peer-reviewed studies if the service was denied as ‘experimental’, and a letter from your doctor explaining why the service was needed.

- File an internal appeal. Submit your appeal in writing to your insurer within 180 days of receiving the denial (or sooner — check your plan). Include a cover letter clearly stating: claim number, denial reason, why you believe coverage should be approved, and all supporting documents.

- Request an External Review if internal appeal fails. Under the ACA, if your internal appeal is denied, you have the right to an external review by an independent organization. File within 60 days of the internal appeal denial. The external reviewer’s decision is binding on your insurer.

- File a complaint with your State Insurance Commissioner. If external review fails or your insurer is not responding, file a complaint with your state’s Department of Insurance. Every state has this office and they have real enforcement power over insurers.

| 💡 Sample Appeal Letter Opening |

| Use this opening for your appeal letter: |

| “I am writing to formally appeal the denial of claim #[CLAIM NUMBER] dated [DATE]. The claim was denied for reason code [CODE] — [DENIAL REASON]. I believe this determination is incorrect for the following reasons: [YOUR REASONS]. I am including supporting documentation from my treating physician, [DR. NAME], confirming the medical necessity of this service.” |

| Keep your letter factual, professional, and specific. Emotional appeals are less effective than medical documentation. |

8. Claim Filing Deadlines — Don’t Miss These

Every health insurance claim has a filing deadline. Missing it means your insurer can legally deny the claim regardless of whether it was valid. These are the standard deadlines:

| Claim Type | Standard Filing Deadline | What Happens If You Miss It |

| In-network claim (filed by provider) | Provider typically files within 24–72 hours | Provider may bill you directly — follow up with provider |

| Out-of-network reimbursement claim | 90 days from date of service (most plans) | Claim denied — no exceptions in most policies |

| Medicare claims | 12 months from date of service | Claim denied permanently |

| Internal appeal | 180 days from denial notice | Right to internal appeal is forfeited |

| External review request | 60 days from internal appeal denial | Right to external review is forfeited |

| Overseas/travel claims | Varies — usually 90 days to 1 year | Check your specific policy’s international claim deadline |

9. Frequently Asked Questions

Q1: How long does it take for a health insurance claim to be processed?

Standard health insurance claims take 14–30 days to process after the insurer receives them. Urgent or emergency claims may be processed faster. If your claim has been pending for more than 30 days, call your insurer’s claims department to check the status. Under the ACA, insurers must process urgent care claims within 72 hours and standard claims within 30 days. State laws may require faster processing — some states mandate 15-day processing.

Q2: What is an EOB and is it the same as a bill?

No — an Explanation of Benefits (EOB) is NOT a bill. It is a summary statement from your insurer showing what was billed by your provider, what the insurer paid, and what portion you are responsible for. An EOB arrives before (or sometimes alongside) your actual bill from the provider. Always wait for your EOB before paying any medical bill — your EOB tells you the correct amount you owe, which may be less than what the provider initially bills you.

Q3: What if my provider says they don’t file insurance claims?

Some providers — particularly cash-pay or concierge practices — do not work directly with insurers. In this case, ask the provider for a ‘superbill’ — a detailed receipt with all the billing codes (CPT and ICD-10 codes) that you need to file a reimbursement claim yourself. Take the superbill, complete your insurer’s reimbursement claim form, and submit both together. Your out-of-network benefits will apply if your plan covers out-of-network care.

Q4: Can I file a health insurance claim for prescriptions?

Usually no — prescription claims are processed at the pharmacy at the time of purchase by entering your insurance information. However, if you paid out of pocket for a prescription (without using your insurance), you can file a manual reimbursement claim with your insurer. Attach your pharmacy receipt showing the drug name, quantity, NDC (National Drug Code), and amount paid. Note that reimbursement is based on your plan’s formulary tier for that drug.

Q5: What does ‘timely filing’ mean on a denial?

A ‘timely filing’ denial means your claim was rejected because it was submitted after your plan’s filing deadline — typically 90 days to 1 year from the date of service, depending on your plan. Unfortunately, timely filing denials are very difficult to overturn on appeal unless you can prove the delay was due to extenuating circumstances (such as a medical emergency or administrative error by the provider). This is why filing claims — or ensuring your provider has filed them — promptly after service is critical.

Q6: How do I file a health insurance claim for mental health services?

Mental health claims are filed the same way as any other medical claim. If your therapist or psychiatrist is in-network, they file on your behalf. If out-of-network, request a superbill from your provider after each session and file a reimbursement claim. Under the ACA’s Mental Health Parity law, insurers must cover mental health services at the same level as physical health services — meaning your deductible, copay, and out-of-pocket limits for mental health must equal those for medical/surgical care. If you’re being charged more for mental health services, that may be an illegal parity violation you can report to your state insurance commissioner.

10. Key Takeaways

| ✅ Everything You Need to Remember |

| In-network providers file claims automatically — you just show your insurance card. Your direct involvement is only needed for out-of-network or reimbursement claims. |

| Always verify in-network status and prior auth BEFORE your appointment — not after. This prevents the most common denial reasons. |

| Never pay a medical bill before reviewing your EOB — billing errors affect 80% of medical bills. Your EOB shows the correct amount you owe. |

| Out-of-network reimbursement claims: get itemized bill → download claim form → fill out completely → attach all documents → submit within 90 days. |

| Denials are not final — 40% of appealed claims are overturned. Always appeal with supporting medical documentation. |

| File deadlines are strict — most plans require claims within 90 days of service. Don’t wait. |

| Keep copies of everything: every bill, EOB, claim form, and insurer communication. You may need them for appeals. |

Sources & References

This article is based on the following authoritative sources:

- Healthcare.gov — Official ACA claim rights and appeals information

- Centers for Medicare & Medicaid Services (CMS) — cms.gov

- National Association of Insurance Commissioners (NAIC) — naic.org

- Consumer Financial Protection Bureau — Medical billing guidance

- U.S. Department of Labor — ERISA claim and appeal regulations

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan is the founder of Claimifio, an independent insurance education publication helping everyday renters, homeowners, and expats understand their coverage rights and claims processes. With a background spanning 8+ years in digital publishing and content research, Imran has spent the last several years studying insurance policy language, policyholder rights, and the gaps between what people think their policy covers — and what it actually pays out. Every guide on Claimifio is researched from primary sources including the Insurance Information Institute, NAIC, and official policy documentation, and written in plain English so you can take action with confidence. Claimifio is an independent educational resource. We are not a licensed insurance agent, broker, or financial advisor. Always consult a licensed professional for advice specific to your situation.

Important Disclaimer: The content on Claimifio.com is for general educational and informational purposes only. We are not licensed insurance agents, brokers, or financial advisors. Nothing here constitutes professional insurance or financial advice. Insurance laws, rates, and requirements vary by state and country. Always consult a licensed insurance professional before making any policy decisions.