Editorial Disclaimer: This article is for general educational purposes only. Claimifio is not a licensed insurance agent or financial advisor. Always consult a licensed professional before making any insurance or financial decisions.

| ⚡ QUICK ANSWER — HMO vs PPO vs EPO vs HDHP |

| HMO (Health Maintenance Organization): Lowest cost, requires a primary care doctor and referrals, no out-of-network coverage. Best for budget-conscious people who stay local. |

| PPO (Preferred Provider Organization): Most flexible, no referrals needed, covers out-of-network care. Best for people who want freedom to see any doctor. |

| EPO (Exclusive Provider Organization): Middle ground — no referrals but no out-of-network coverage. Good balance of cost and flexibility. |

| HDHP (High Deductible Health Plan): Lowest premium, highest deductible, pairs with a tax-free Health Savings Account (HSA). Best for healthy people who rarely need care. |

| The bottom line: choose HMO for the lowest cost, PPO for maximum flexibility, EPO for a balance, or HDHP if you want to save on premiums and build a medical emergency fund. |

1. Why Does Your Health Plan Type Matter So Much?

When Americans choose health insurance — whether through their employer, the ACA Marketplace, or a private plan — they don’t just choose a price. They choose a structure that determines which doctors they can see, whether they need referrals, how much they pay per visit, and what happens if they go outside the plan’s network.

Choosing the wrong plan type can cost you thousands of dollars annually — or mean you can’t see the doctor you want without paying out of pocket. The good news: once you understand the four main plan types, the decision becomes much clearer.

| 💡 Key Insight |

| The four plan types differ on three core dimensions: |

| 1. COST — How much you pay in premiums and per visit |

| 2. FLEXIBILITY — Whether you need referrals, which doctors you can see |

| 3. NETWORK — Whether out-of-network care is covered at all |

| Understanding where each plan sits on these three dimensions is the entire decision. |

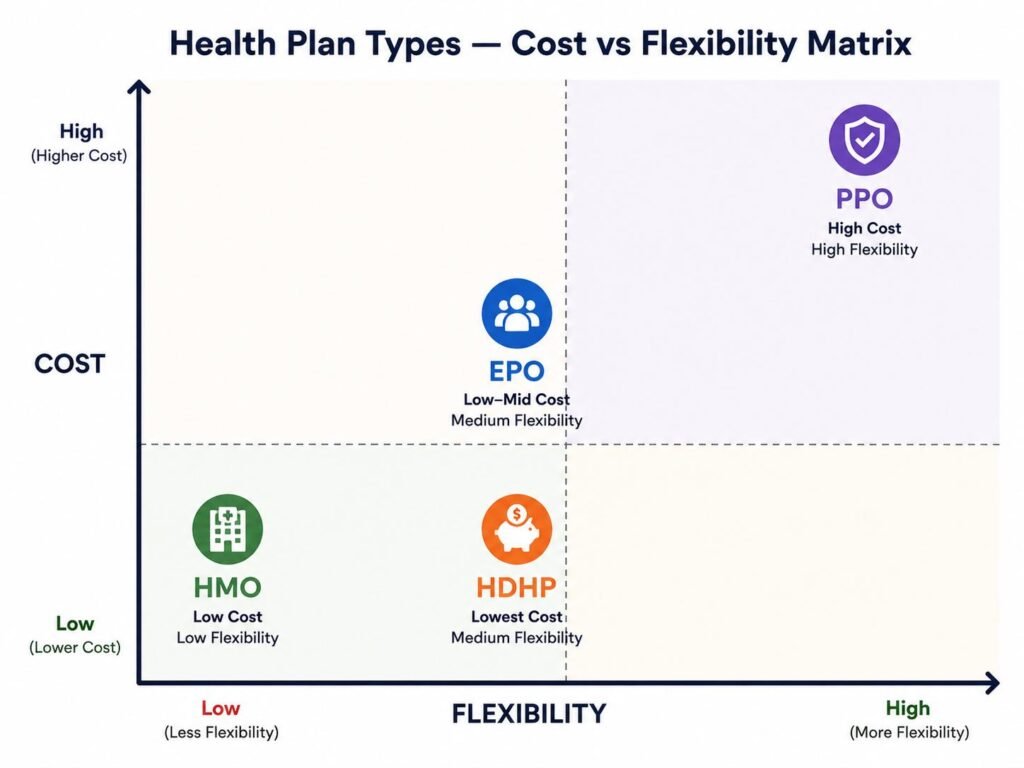

2. The Four Plan Types — Quick Visual Overview

| 🔵 HMO — Health Maintenance Organization Best for: Low cost, coordinated care, staying in-network |

| Monthly Premium: Lowest of the four plan types |

| Deductible: Usually lower — some HMOs have $0 deductible |

| Need a Primary Care Doctor (PCP): Yes — required |

| Need Referrals for Specialists: Yes — must come from your PCP |

| Out-of-Network Coverage: None (except genuine emergencies) |

| Best For: Budget-conscious, healthy individuals who have a doctor they trust and don’t need specialists often |

| 🟢 PPO — Preferred Provider Organization Best for: Maximum flexibility, specialist access, frequent travelers |

| Monthly Premium: Highest of the four plan types |

| Deductible: Moderate — in-network lower than out-of-network |

| Need a Primary Care Doctor (PCP): No — optional |

| Need Referrals for Specialists: No — see any specialist directly |

| Out-of-Network Coverage: Yes — at higher cost sharing |

| Best For: People managing chronic conditions, frequent travelers, those who want to keep specific doctors |

| 🟡 EPO — Exclusive Provider Organization Best for: Mid-range cost with no referral requirement |

| Monthly Premium: Mid-range — lower than PPO, similar to or slightly above HMO |

| Deductible: Moderate |

| Need a Primary Care Doctor (PCP): No — optional |

| Need Referrals for Specialists: No — see specialists directly |

| Out-of-Network Coverage: None (except genuine emergencies) |

| Best For: People who want PPO-style flexibility without the high premium, but are comfortable staying in-network |

| 🟣 HDHP — High Deductible Health Plan Best for: Healthy people, tax savings via HSA, lowest monthly premium |

| Monthly Premium: Lowest — often cheaper than HMO |

| Deductible: High — minimum $1,650 individual / $3,300 family in 2026 |

| Need a Primary Care Doctor (PCP): Depends on whether it’s an HMO-style or PPO-style HDHP |

| Need Referrals for Specialists: Depends on underlying plan structure |

| Out-of-Network Coverage: Depends on underlying plan structure |

| HSA Eligibility: Yes — the only plan type that qualifies for a Health Savings Account |

| Best For: Healthy, young adults with savings who want to minimize monthly costs and build an HSA |

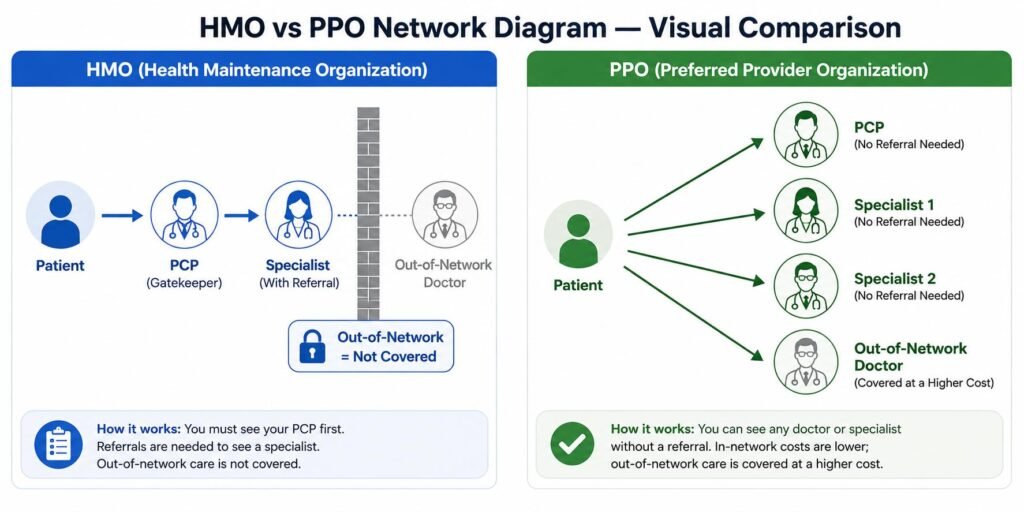

3. HMO — Health Maintenance Organization: Full Explanation

An HMO is a managed care plan built around a coordinated, gatekeeper model. You choose one Primary Care Physician (PCP) from the plan’s network — this doctor becomes your central point of contact for all healthcare. If you need to see a specialist, your PCP must issue a referral first. Without a referral, the visit is not covered.

How an HMO Works in Practice

- You choose a PCP from your HMO’s provider directory when you enroll.

- You see your PCP for all routine care, annual exams, and any new health concern.

- Your PCP refers you to an in-network specialist if needed.

- All care must be in-network — HMOs do not cover out-of-network providers except genuine emergencies.

- Lower premiums and copays reward you for staying within the coordinated system.

HMO Pros & Cons

| HMO Advantages | HMO Disadvantages |

| Lowest monthly premiums | No out-of-network coverage (except emergencies) |

| Lower copays and out-of-pocket costs | Must get referrals to see specialists |

| Lower or zero deductibles on many plans | Less flexibility in choosing providers |

| Coordinated care reduces duplicate tests | Changing your PCP requires paperwork |

| Predictable costs — easy to budget | If you travel frequently, coverage gaps are a risk |

4. PPO — Preferred Provider Organization: Full Explanation

A PPO gives you maximum freedom. You can see any doctor — primary care or specialist — without a referral. You can go in-network for lower costs or out-of-network for higher costs. There is no gatekeeper. The trade-off: PPOs have significantly higher monthly premiums than HMOs.

How a PPO Works in Practice

- No PCP required — you can see any doctor in the network directly without a primary care referral.

- See specialists directly — book a dermatologist, cardiologist, or orthopedist without waiting for a referral from a GP.

- In-network care costs less — you pay lower deductibles and coinsurance when using network providers.

- Out-of-network care is covered — but at higher cost sharing. Your insurer pays less and you pay more.

- Higher premiums — you pay for this flexibility in your monthly bill, regardless of whether you use it.

PPO Pros & Cons

| PPO Advantages | PPO Disadvantages |

| Maximum flexibility — see any doctor | Highest monthly premiums |

| No referrals needed for specialists | Higher deductibles than HMOs |

| Out-of-network care partially covered | More complex cost structure |

| Ideal for people with multiple specialists | Easy to accidentally incur large out-of-network bills |

| Best for frequent travelers and expats | Can lead to fragmented care without a coordinating PCP |

5. EPO — Exclusive Provider Organization: Full Explanation

An EPO is a hybrid plan that combines the best features of HMO and PPO plans. Like a PPO, an EPO does not require referrals — you can see specialists directly. Like an HMO, an EPO only covers in-network care (except emergencies). The result is a plan that is more flexible than an HMO and more affordable than a PPO.

How an EPO Works in Practice

- No PCP required — you can see any in-network doctor without a primary care referral.

- No referrals for specialists — direct access to in-network specialists without going through a gatekeeper.

- In-network only — like HMOs, EPOs provide no out-of-network coverage except genuine emergencies.

- Mid-range premiums — generally lower than PPOs but comparable to or slightly above HMOs.

EPO Pros & Cons

| EPO Advantages | EPO Disadvantages |

| No referrals needed — more flexible than HMO | No out-of-network coverage (except emergencies) |

| Lower premiums than PPO | Network can be smaller than PPOs |

| Direct specialist access | No coverage if you travel outside your service area |

| Good balance of cost and flexibility | Less common than HMO and PPO — fewer plan options |

| No PCP requirement | Not available in all states or from all insurers |

6. HDHP + HSA — High Deductible Health Plan: Full Explanation

An HDHP is defined not by its network structure but by its deductible level. In 2026, the IRS defines an HDHP as any plan with a minimum deductible of $1,650 for individuals or $3,300 for families. The key benefit of an HDHP is eligibility for a Health Savings Account (HSA) — a powerful tax-advantaged account that can save you thousands.

What Is an HSA and Why Does It Matter?

A Health Savings Account (HSA) is a special savings account that only HDHP enrollees can open. Money contributed to an HSA is triple tax-advantaged:

- Tax-deductible contributions: Every dollar you put in reduces your taxable income.

- Tax-free growth: Interest and investment gains grow without being taxed.

- Tax-free withdrawals: Withdrawals for qualified medical expenses are completely tax-free.

| HSA Facts for 2026 | Individual | Family |

| Minimum HDHP deductible to qualify | $1,650 | $3,300 |

| Maximum HSA contribution limit | $4,300 | $8,550 |

| Catch-up contribution (age 55+) | +$1,000 | + $1,000 |

| Does money roll over year to year? | Yes — forever | Yes — forever |

| Can it be invested (stocks/funds)? | Yes | Yes |

HDHP Pros & Cons

| HDHP Advantages | HDHP Disadvantages |

| Lowest monthly premium of all plan types | High deductible — large out-of-pocket exposure |

| HSA triple tax advantage | Must pay full deductible before most coverage kicks in |

| HSA funds roll over — never expire | Poor fit for people with frequent medical needs |

| HSA can be invested like a retirement account | Requires financial discipline and savings buffer |

| Premium savings can fund your HSA | Preventive care is free — but most other care isn’t until deductible met |

7. The Ultimate Comparison Table: HMO vs PPO vs EPO vs HDHP

Here is the complete side-by-side comparison of all four plan types across every important dimension:

| Feature | 🔵 HMO | 🟢 PPO | 🟡 EPO | 🟣 HDHP |

| Monthly Premium | Lowest | Highest | Mid-range | Lowest (often lower than HMO) |

| Deductible | Low (some = $0) | Moderate | Moderate | High ($1,650+ individual) |

| Need Primary Care Doctor? | ✅ Yes — required | ❌ No — optional | ❌ No — optional | Depends on plan structure |

| Need Referrals? | ✅ Yes — from PCP | ❌ No | ❌ No | Depends on plan structure |

| In-Network Coverage | ✅ Full coverage | ✅ Full coverage | ✅ Full coverage | ✅ Full coverage |

| Out-of-Network Coverage | ❌ None* | ✅ Partial coverage | ❌ None* | Depends on plan structure |

| HSA Eligible? | ❌ No | ❌ No | ❌ No | ✅ Yes — only HDHP qualifies |

| Best Cost Scenario | Use in-network regularly | Manage chronic conditions | Direct specialist access | Rarely need medical care |

| Worst Cost Scenario | Need out-of-network care | High premium if rarely need care | Need out-of-network care | Frequent medical needs |

| Overall Flexibility | Low | High | Medium | Medium |

* Emergency care is always covered regardless of network, under federal law.

8. Real Cost Comparison — Same Person, Four Plans

Meet Sarah — a 32-year-old non-smoker in Texas, moderately healthy, who visits her doctor 4 times per year and has one specialist visit annually. Here is what each plan type would cost her in a typical year:

| Cost Category | HMO | PPO | EPO | HDHP + HSA |

| Monthly Premium | $310 | $485 | $385 | $265 |

| Annual Premium Total | $3,720 | $5,820 | $4,620 | $3,180 |

| Annual Deductible | $500 | $800 | $750 | $2,500 |

| 4 PCP visits (copay/coinsurance) | $120 ($30 copay x4) | $180 ($45 copay x4) | $140 ($35 copay x4) | $600 (pre-deductible) |

| 1 Specialist visit | $60 (with referral) | $250 (no referral needed) | $90 (no referral) | $300 (pre-deductible) |

| Annual Lab Work | $0 (in-network) | $100 | $50 | $200 (pre-deductible) |

| TOTAL Annual Cost (typical year) | ~$4,400 | ~$7,150 | ~$5,650 | ~$6,780 |

| TOTAL if major illness ($15,000 bill) | ~$5,400 | ~$8,400 | ~$6,700 | ~$9,680 |

| HSA Tax Savings (if HDHP) | N/A | N/A | N/A | ~$860 (20% tax bracket) |

| Effective HDHP Cost with HSA savings | N/A | N/A | N/A | ~$5,920 after tax savings |

| 💡 What This Example Shows |

| For a moderately healthy person like Sarah, the HMO wins on total annual cost in a typical year ($4,400) — even though its deductible isn’t zero. |

| The PPO costs nearly $2,750 more per year than the HMO — that ‘flexibility premium’ is real money. |

| The HDHP becomes competitive when you factor in HSA tax savings AND the fact that HSA money rolls over every year — essentially a medical retirement account. |

| These are estimates — your actual costs depend on your specific plan, location, and health usage. |

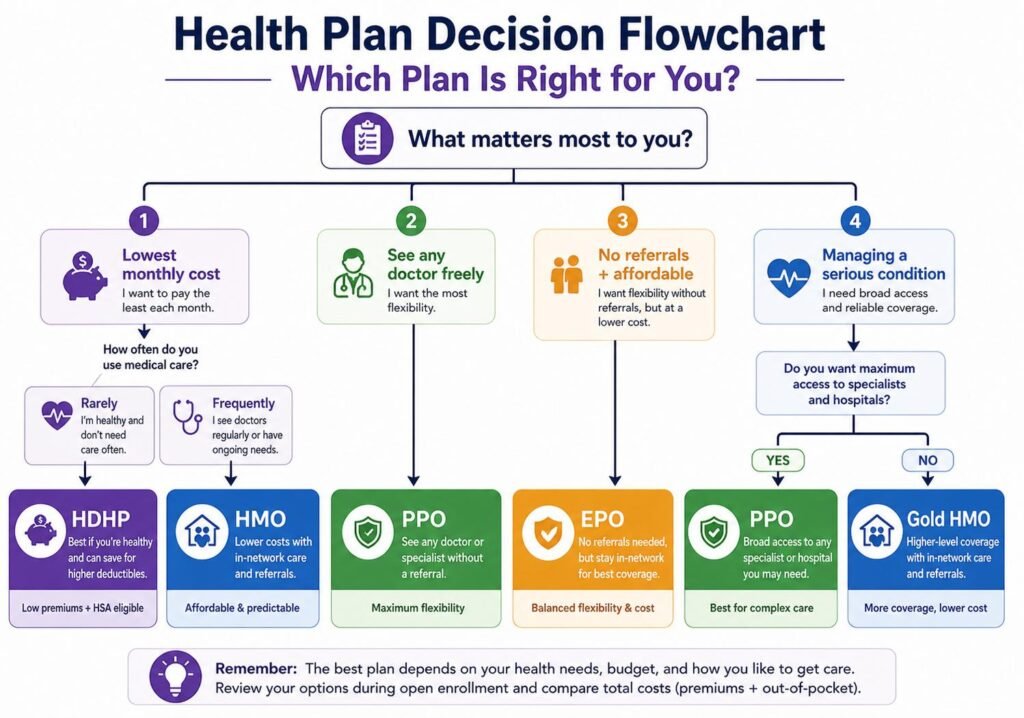

9. Which Plan Is Right for You? Decision Guide

Answer these questions about your situation and match yourself to the right plan:

YOUR SITUATION → BEST PLAN → WHY

| Your Situation | Best Plan | Why |

| You want the absolute lowest monthly premium | HDHP | Lowest premium of all plan types — pair with HSA to offset high deductible |

| You want lowest total annual cost and rarely travel | HMO | Lowest premiums + lowest copays when staying in-network |

| You have a specific specialist you must keep seeing | PPO | Only PPO covers out-of-network specialists — no referral needed |

| You are managing a chronic condition | PPO or Gold HMO | Frequent care = higher deductible plans become expensive; PPO gives specialist access |

| You are young and healthy with $3,000+ savings | HDHP + HSA | Low premium + build tax-free medical savings for the future |

| You want to see specialists without referrals but stay in-network | EPO | No referrals + no out-of-network = best balance between HMO and PPO |

| You travel frequently for work | PPO | HMO/EPO leave you uncovered away from home; PPO works nationwide |

| You qualify for ACA Cost Sharing Reductions (CSRs) | Silver HMO or Silver PPO | CSRs are only available on Silver plans — dramatically reduce deductible/copay |

| You are pregnant or planning to start a family | PPO or Gold HMO | Maternity costs are high — lower deductible and out-of-pocket max protects you |

| You just want simplicity and one doctor who knows you | HMO | PCP model = coordinated, simple, lower cost |

10. Frequently Asked Questions

| 📌 SEO Note |

| Add all 6 questions below into Rank Math’s FAQ Schema block. These appear as expandable Q&As directly in Google search results — significantly increasing click-through rate for this comparison article. |

Q1: Which is better — HMO or PPO?

Neither is universally better — the right choice depends entirely on your situation. HMOs are better if you want the lowest cost, have a primary care doctor you trust, and don’t need to see specialists often. PPOs are better if you want the freedom to see any doctor without a referral, have ongoing specialist needs, or travel frequently. For most healthy, budget-conscious individuals, an HMO saves $1,500–$2,500 per year compared to a PPO. For people managing complex or chronic conditions who need frequent specialist access, a PPO’s flexibility often justifies the higher premium.

Q2: Can I switch from an HMO to a PPO mid-year?

Generally, no. Health plan enrollment changes are restricted to your annual open enrollment period (typically October–November for employer plans, or November 1–January 15 for ACA Marketplace plans). The only exception is a qualifying life event — such as losing your job, getting married, having a baby, or moving to a new state — which triggers a Special Enrollment Period during which you can change your plan. Outside of these windows, you’re locked into your plan type until the next enrollment period.

Q3: Does an EPO cover emergency care out of network?

Yes — under federal law, all health insurance plans including EPOs and HMOs must cover genuine emergency care regardless of whether the provider is in-network. If you’re in a life-threatening emergency and receive care at an out-of-network facility, your plan must cover it at in-network rates (you cannot be charged more for emergencies). However, ’emergency’ has a specific definition — follow-up care after the emergency, or non-urgent care at an out-of-network facility, is not covered by EPO or HMO plans.

Q4: Can I have both an HMO and an HSA?

No — only HDHP plan enrollees are eligible to contribute to a Health Savings Account. HMOs, PPOs, and EPOs generally do not qualify for HSA eligibility because their deductibles are usually below the IRS minimum threshold ($1,650 for individuals in 2026). If you have an HMO, you may be eligible for a Flexible Spending Account (FSA) instead — but FSAs have a ‘use it or lose it’ rule unlike HSAs, and the contribution limit is lower ($3,300 in 2026 for FSAs).

Q5: What happens if I accidentally see an out-of-network doctor with an HMO?

With an HMO, seeing an out-of-network provider (except in a genuine emergency) typically means you receive no insurance coverage — you are responsible for the full bill at the provider’s normal rates, which can be very high. This is one of the most common and costly HMO mistakes. Before every appointment, always verify your provider is in-network by calling your insurer directly — provider directories are not always current. If you’re told a doctor is in-network and they turn out not to be, you may be able to dispute the claim under surprise billing protections.

Q6: Is HDHP good for families?

HDHPs can be excellent for families — or very risky — depending on the family’s health situation. A healthy family with children who rarely need care beyond annual check-ups can save significantly: lower premiums free up money to fund an HSA, and preventive care (vaccines, well-child visits) is covered free on all plans including HDHPs. However, families with a member who has a chronic condition, requires frequent specialist visits, or has ongoing prescription needs often find HDHPs expensive — the high deductible can be reached quickly when multiple family members need care.

11. Key Takeaways

| ✅ Everything You Need to Remember |

| HMO = Lowest cost, most restricted. Requires PCP and referrals. No out-of-network coverage. Best for budget-focused, locally-based, healthy individuals. |

| PPO = Most flexible, most expensive. No referrals, covers out-of-network. Best for specialist access, chronic conditions, frequent travelers. |

| EPO = Best middle ground. No referrals but no out-of-network coverage. Good balance of cost and flexibility for people comfortable staying in-network. |

| HDHP = Lowest premium, highest deductible. Qualifies for HSA — triple tax-advantaged medical savings account. Best for healthy, savings-ready individuals. |

| Real cost comparison: HMO wins for typical annual cost. HDHP wins long-term if you stay healthy and build your HSA. PPO costs $1,500–$3,000+ more per year than HMO. |

| The decision boils down to three questions: (1) How much can I afford monthly? (2) How often will I actually need care? (3) Do I need specific doctors or out-of-network access? |

| Always verify your doctors are in-network before enrolling in any plan — especially HMO or EPO, where out-of-network means no coverage. |

Sources & References

This article is based on the following authoritative sources:

- Healthcare.gov — Official ACA plan type explanations

- Kaiser Family Foundation (KFF) — kff.org — Employer health benefits survey 2025

- National Association of Insurance Commissioners (NAIC) — naic.org

- IRS.gov — HSA contribution limits and HDHP definitions for 2026

- Centers for Medicare & Medicaid Services (CMS) — cms.gov

| 📚 Read Next on Claimifio |

| → Health Insurance in the USA: Complete Beginner’s Guide (2026) ← Full overview of the US health system |

| → How to File a Health Insurance Claim: Step-by-Step |

| → Health Insurance Open Enrollment 2026: Dates, Deadlines & How to Choose |

| → Freelancer Health Insurance USA: Full 2026 Guide |

| → What Is an Insurance Deductible? Simple Explanation |

| → How to Appeal a Denied Insurance Claim (Any Type) |

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan is the founder of Claimifio, an independent insurance education publication helping everyday renters, homeowners, and expats understand their coverage rights and claims processes. With a background spanning 8+ years in digital publishing and content research, Imran has spent the last several years studying insurance policy language, policyholder rights, and the gaps between what people think their policy covers — and what it actually pays out. Every guide on Claimifio is researched from primary sources including the Insurance Information Institute, NAIC, and official policy documentation, and written in plain English so you can take action with confidence. Claimifio is an independent educational resource. We are not a licensed insurance agent, broker, or financial advisor. Always consult a licensed professional for advice specific to your situation.

Important Disclaimer: The content on Claimifio.com is for general educational and informational purposes only. We are not licensed insurance agents, brokers, or financial advisors. Nothing here constitutes professional insurance or financial advice. Insurance laws, rates, and requirements vary by state and country. Always consult a licensed insurance professional before making any policy decisions.