Editorial Disclaimer: This article is for general educational purposes only. Claimifio is not a licensed insurance agent or financial advisor. Always consult a licensed professional before making any insurance or financial decisions.

Panic, Property, and Policies: Understanding Mold Removal Costs

Few things strike fear into a homeowner’s heart quite like discovering mold. That musty smell, the unsightly discoloration – it signals not just a potential health hazard, but also the dreaded prospect of expensive remediation. According to industry estimates, mold removal can cost anywhere from a few hundred dollars for small spots to tens of thousands for widespread infestations. This immediately begs the question: Does Home Insurance Cover Mold Removal?

The short answer, as with many things in insurance, is: It depends. Unlike fire or wind damage, mold coverage isn’t straightforward. It hinges almost entirely on what caused the mold. This guide will break down the complexities of homeowners insurance mold coverage, clarifying when your policy might step in, what to expect regarding costs and limits, and how to protect your home (and your wallet) from this unwelcome invader.

1. The Core Rule: When Does Insurance Cover Mold?

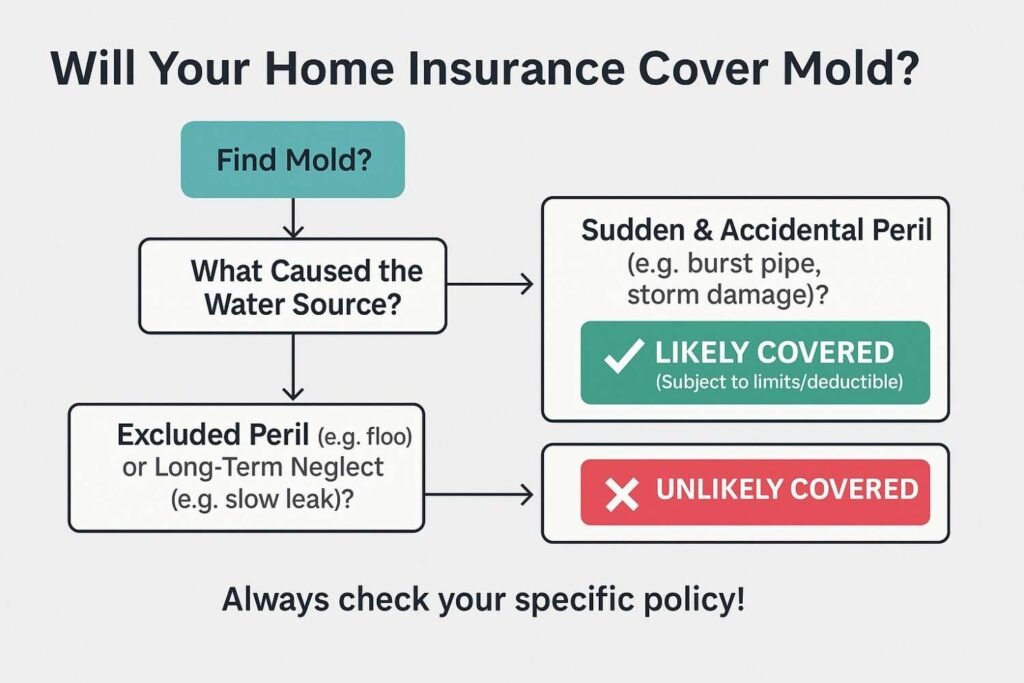

The fundamental principle governing Home Insurance Cover Mold Removal revolves around the cause of the water damage that led to the mold growth. Your standard homeowners policy (HO-3) generally covers “sudden and accidental” perils.

Mold Coverage: Yes, If Caused By a Covered Peril

Mold damage is typically covered IF it resulted from a peril explicitly covered by your policy, and the damage was “sudden and accidental.” This often includes:

- Sudden Pipe Burst: A frozen pipe bursting behind a wall, causing a sudden flood.

- Accidental Overflow: An overflowing bathtub or toilet (not due to neglect).

- Storm-Related Damage: A tree falling on your roof during a storm, causing a hole through which rain enters, leading to mold.

- Fire Extinguishing: Water damage from firefighters putting out a covered fire.

- Vandalism: Water damage caused by vandals.

In these scenarios, your policy would likely cover not only the initial water damage and the repairs, but also the subsequent mold remediation costs insurance typically covers, up to specific limits.

Mold Coverage: No, If Caused By Excluded Perils or Neglect

Your policy will generally NOT cover mold damage if it stems from:

- Flooding: Water entering your home from outside (e.g., river overflow, storm surge) is covered by separate flood insurance, not standard homeowners. (Even if covered by flood insurance, mold coverage may be separate and limited).

- Sewer Backups/Sump Pump Failure: Unless you have an specific endorsement (add-on) for this.

- Long-Term Leaks or Neglect: This is a big one. A slow, dripping pipe behind a wall that goes unnoticed for months, or poor home maintenance that leads to chronic moisture issues, will typically be excluded. Insurers consider this a preventable issue that falls under homeowner responsibility.

- High Humidity/Condensation: General moisture in the air that leads to mold is usually not covered.

This distinction between “sudden and accidental” versus “long-term maintenance issues” is the most crucial factor in determining when does insurance cover mold.

Hypothetical Scenario A: Sudden Pipe Burst (Covered)

In Dallas, TX, Sarah returns from a weekend trip to find her downstairs ceiling dripping. A pipe in an upstairs bathroom unexpectedly burst, causing significant water damage to the ceiling, drywall, and a subsequent mold bloom within days. Because the pipe burst was “sudden and accidental,” her homeowners policy would likely cover the water damage repair, the cost to remove and replace the moldy drywall, and professional mold removal insurance (subject to her deductible and policy limits).

2. Unpacking Coverage Limits and Endorsements for Mold Damage Claims

Even when homeowners insurance mold coverage is available, it’s vital to understand that it often comes with specific limitations.

Typical Coverage Limits for Mold Damage

Most standard homeowners policies have sub-limits for mold remediation. This means that while your dwelling coverage might be $300,000, the amount your insurer will pay for mold specifically might be much lower – commonly $5,000 to $10,000. These limits apply even if the overall water damage claim (which is covered) is much higher. If your mold remediation exceeds this sub-limit, you’ll be responsible for the difference.

- Example: A sudden pipe burst causes $15,000 in water damage repairs and $8,000 in mold remediation. If your mold sub-limit is $5,000, your insurer would pay $15,000 for water damage + $5,000 for mold, leaving you to pay the remaining $3,000 for mold remediation out of pocket (plus your deductible).

Enhancing Your Coverage: Mold Endorsements

If you’re concerned about these low sub-limits, some insurers offer mold endorsements (also called riders or add-ons) that you can purchase to increase your mold coverage. These endorsements can raise the limit to $25,000, $50,000, or even higher, providing significantly more protection. This is an important consideration, especially if you live in a humid climate or an older home prone to moisture issues.

Get ready for unforeseen events by learning more about Home Insurance Claim Process After Storm Damage.

Hypothetical Scenario B: Long-Term Leak (Not Covered)

A homeowner in Atlanta, GA, discovers a large patch of black mold spreading on their bathroom wall. Upon investigation, they realize it’s been caused by a slow, persistent leak from the shower pan that has been present for over a year. Despite the significant damage and high mold remediation costs insurance would normally cover if sudden, their homeowners policy would likely deny this claim. The insurer would categorize this as damage due to “neglect” or “lack of maintenance,” a common exclusion for is mold damage covered by homeowners insurance.

3. The Mold Damage Claim Process: What to Do

If you suspect mold and believe it stems from a covered peril, acting quickly and strategically is key for a successful mold damage claim process.

Your Action Plan:

- Stop the Source: Your absolute first step is to stop the water source immediately. If it’s a burst pipe, turn off the main water supply.

- Document Everything: This is crucial.

- Take Photos & Videos: Document the water source, the extent of the water damage, and the visible mold before any cleanup.

- Keep Receipts: Save receipts for any immediate mitigation efforts (e.g., fans, dehumidifiers, leak repair parts).

- Contact Your Insurance Agent/Provider: Notify them as soon as possible. Explain the cause of the water damage and the subsequent mold discovery.

- Mitigate Further Damage (Safely!): While waiting for an adjuster, remove standing water, dry out affected areas (if safe to do so), and ventilate. However, do NOT try to clean extensive mold yourself, especially black mold, without professional guidance, as you could spread spores or expose yourself to health risks.

- Get Professional Assessments: Your insurer may send an adjuster. You may also consider getting an independent mold inspection to assess the extent of the growth and necessary remediation.

- Understand Your Policy: Re-read your policy’s section on water damage and mold, paying attention to coverage limits and exclusions.

Water damage mold coverage claims require diligence and quick action. Delaying can lead to your insurer arguing the mold grew due to your inaction.

For valuable guidelines on mold cleanup in your home and how to prevent it, consult the Environmental Protection Agency (EPA)’s official mold resources.

4. Prevention is Key: Reducing Your Risk (and Claim Stress)

The best claim is the one you never have to make. Preventing mold is far easier (and cheaper) than remediation, and it directly impacts whether Home Insurance Cover Mold Removal for you.

- Fix Leaks Promptly: Don’t delay repairing leaky faucets, pipes, or roof issues. Even small drips can lead to significant mold over time.

- Manage Humidity: Use dehumidifiers in damp areas like basements or bathrooms. Ensure proper ventilation.

- Improve Airflow: Keep doors to closets open occasionally, and move furniture away from walls to allow air circulation.

- Proper Ventilation: Use exhaust fans in bathrooms and kitchens.

- Clean & Dry Immediately: If you experience any water spill or minor leak, clean it up thoroughly and dry the area within 24-48 hours.

- Regular Inspections: Periodically check under sinks, around toilets, in basements/attics, and behind appliances for any signs of moisture or leaks.

By being proactive, you not only reduce your chance of needing to claim but also keep your home healthier and more valuable.

For more comprehensive information on homeowners insurance in the US, including common coverages and how policies work, consult the National Association of Insurance Commissioners (NAIC) consumer guides.

FAQ: Does Home Insurance Cover Mold Removal?

Q: Does black mold automatically mean my insurance won’t cover it?

A: No, the type of mold (e.g., black mold) doesn’t directly determine coverage. What matters is the cause of the water that led to the mold. If the water damage was from a sudden, covered peril, black mold remediation could be covered.

Q: What is the typical coverage limit for mold remediation?

A: Standard homeowners policies often have low sub-limits for mold, commonly ranging from $1,000 to $10,000. It’s crucial to check your specific policy or consider purchasing a mold endorsement for higher limits.

Q: Can I prevent mold from growing after a covered water event?

A: Yes, and you should! Your policy usually requires you to take reasonable steps to prevent further damage. This includes promptly drying out the area, using fans/dehumidifiers, and removing damaged porous materials if safe to do so.

Q: What if I didn’t know about the slow leak that caused the mold?

A: Unfortunately, ignorance is not typically an excuse for insurance purposes. Insurers usually expect homeowners to maintain their property. If a leak was slow and could have been detected with reasonable diligence, it often falls under the “neglect” exclusion.

Q: Should I get a mold inspection before filing a claim?

A: You can, but often your insurer will send an adjuster to assess the damage. If you’re unsure of the cause, an independent mold inspection might help determine if the origin falls under a covered peril, but discuss this with your agent first.

Don’t Let Mold Undermine Your Home’s Value and Your Health

Finding mold in your home is stressful, but understanding your homeowners insurance mold coverage doesn’t have to be. The key takeaway is clear: the cause of the water intrusion is everything. Act swiftly to address water issues, meticulously document any damage, and communicate openly with your insurance provider.

Protecting your home from mold isn’t just about repairs; it’s about safeguarding your health and your property’s long-term value. Be proactive in prevention, and be prepared by knowing the specifics of your policy.

Don’t wait for mold to appear. Review your homeowners insurance policy today to understand your mold coverage limits and consider an endorsement for enhanced protection!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan is the founder of Claimifio, an independent insurance education publication helping everyday renters, homeowners, and expats understand their coverage rights and claims processes. With a background spanning 8+ years in digital publishing and content research, Imran has spent the last several years studying insurance policy language, policyholder rights, and the gaps between what people think their policy covers — and what it actually pays out. Every guide on Claimifio is researched from primary sources including the Insurance Information Institute, NAIC, and official policy documentation, and written in plain English so you can take action with confidence. Claimifio is an independent educational resource. We are not a licensed insurance agent, broker, or financial advisor. Always consult a licensed professional for advice specific to your situation.

Important Disclaimer: The content on Claimifio.com is for general educational and informational purposes only. We are not licensed insurance agents, brokers, or financial advisors. Nothing here constitutes professional insurance or financial advice. Insurance laws, rates, and requirements vary by state and country. Always consult a licensed insurance professional before making any policy decisions.