The $1 Million Mistake: The “Business Activity” Exclusion

The rise of platforms like Airbnb, Vrbo, and HomeAway has revolutionized real estate investment and travel, allowing property owners to easily generate substantial Home Insurance for Rental Income. However, for every dollar earned, there is an invisible, growing risk: the near-certainty that your standard US Homeowner’s Insurance Policy (HO-3) will not cover you when things go wrong.

The heart of the problem lies in the insurance industry’s foundational rule: A homeowner’s policy is designed to cover personal residential risk, not business commercial activity.

When you rent your home or a room for a fee, even for a single night, an insurer views that transaction as a business activity. Most standard US HO-3 policies contain a Business Activity Exclusion—a clause stating that coverage for property damage or liability claims resulting from commercial or business operations conducted on the premises is severely limited or entirely void.

What does this mean for you? If a paying guest slips, falls, and sues you for $500,000, or if a guest causes a fire resulting in $100,000 in damage, your personal insurance carrier has a clear contractual basis to deny the claim, leaving you solely responsible.

This guide breaks down the massive Host Protection Insurance Gap and outlines the essential steps to protect your property and personal assets when listing on short-term rental platforms.

1. The Three Primary Gaps in Standard HO-3 Coverage

Your homeowner’s policy falls apart in three key areas the moment you welcome a paying short-term guest:

A. The Liability Gap (The Most Costly Risk)

Liability is the greatest exposure for any host. A standard HO-3 policy provides Personal Liability coverage, but this coverage often ends when the injury is related to a business purpose.

- The Scenario: A guest trips over a loose rug or falls off a swing set and requires surgery. They sue you for negligence.

- The Policy Response: The insurer claims the injury arose from your commercial venture (the rental business) and denies the claim, forcing you to pay for your own legal defense and any resulting judgment.

B. The Property Damage Gap

While an HO-3 policy covers property damage from common perils (fire, windstorm, hail), many contain exclusions for damage caused by tenants, occupants, or renters.

- The Scenario: A guest throws a party, resulting in severe vandalism, broken fixtures, or intentional damage to the interior walls.

- The Policy Response: The insurer may deny the claim because the damage was caused by a paying renter, not a covered peril like a storm.

C. The Contents & Theft Gap

Standard policies often have a very low limit (often just $2,500) for personal property used for business purposes. Furthermore, theft is frequently excluded when committed by a person (a tenant) legally allowed into the home.

- The Scenario: A guest steals electronics, expensive linens, or even art from the rental property.

- The Policy Response: Theft by a tenant is generally not a covered peril under standard theft provisions, leaving the host without recourse through their HO-3.

2. Platform Protection: The “AirCover” Reality

Platforms like Airbnb offer hosts protection programs, but they are not a substitute for your own insurance policy.

AirCover for Hosts (Airbnb)

Airbnb’s AirCover (which includes Host Damage Protection and Host Liability Insurance) is complimentary and offers protection up to a certain limit ($3 million in damage protection and $1 million in liability).

| Coverage | Platform Protection (AirCover) | Specialized Host Insurance (Recommended) |

| Nature of Coverage | Protection Program/Secondary Insurance (excess & surplus) | Primary, underwritten Insurance Policy |

| Key Exclusions | Normal wear and tear, pet damage (often limited), income loss from maintenance. | Can cover guest-caused damage, theft, and malicious acts. |

| Claim Payout | Often pays Actual Cash Value (depreciated value). | Better policies offer Replacement Cost Coverage. |

| Income Loss | Typically does not cover lost rental income from extended repairs. | Includes Loss of Income (Business Interruption). |

The Host Protection Insurance Gap: The platform’s coverage is usually secondary and may not guarantee payment. If an insurer views your activity as high-risk, a platform’s guarantee might be their only defense, which is far less reliable than a true, regulated insurance policy. Furthermore, platform protection often has deductibles and exclusions you must adhere to.

Hosts should always review the official terms and conditions of their chosen platform. For the most up-to-date details on Airbnb’s liability programs, review their official site’s “AirCover” or “Host Protection” documentation.

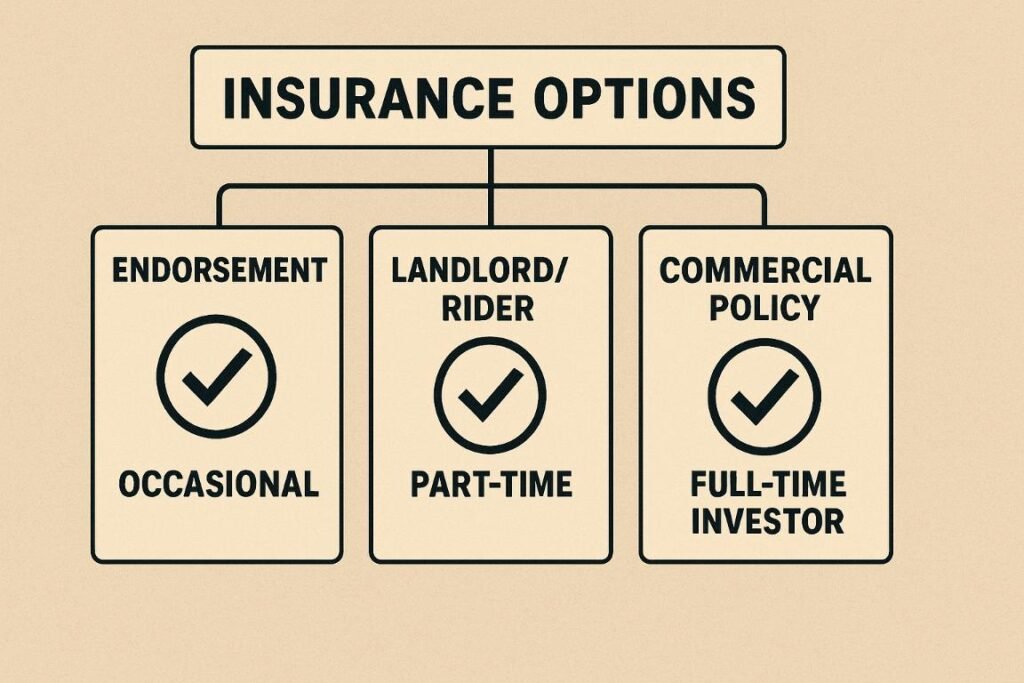

3. The Real Solutions: Your Coverage Options

To effectively mitigate the risk and protect your Home Insurance for Rental Income business, you have three primary insurance options, depending on your property’s usage:

A. Home Insurance Endorsement (The Limited Solution)

Some traditional insurers offer a Home Sharing Endorsement or rider that can be added to your HO-3 policy.

- Best For: Hosts who rent very occasionally (e.g., fewer than 30 nights per year) while they are still living in the home.

- Limitation: This is a limited solution. It raises the liability coverage and property damage limits for short-term stays, but typically won’t cover long-term, frequent, or full-time rental activity.

B. Landlord Policy (DP-3) with a Short-Term Rental Rider (The Middle Ground)

The Landlord Policy (DP-3) is designed for properties with long-term tenants (e.g., 6+ months). However, some specialty carriers allow you to add a Short-Term Rental Endorsement to this policy.

- Best For: Owners who primarily use the property as a rental but may occasionally use it themselves (or keep it vacant for periods).

- This policy is similar to what US citizens need when living abroad:The Expat Landlord Guide: Home Insurance for Renting Out Your US Home While Living Abroad.

C. Specialized Commercial/Business Policy (The Comprehensive Solution)

This is a dedicated insurance product specifically designed for vacation rental properties. It is often referred to as Vacation Rental Insurance or a Business Owners Policy (BOP) tailored for short-term rentals.

- Best For: Full-time investors or owners who rent the property out year-round.

- Key Feature: This policy is written on a commercial form, which eliminates the “business activity exclusion.” It includes Commercial General Liability and Business Interruption Coverage (Loss of Income) that pays out if a covered loss prevents you from accepting bookings.

4. The Critical Component: Loss of Income Coverage

As an expat or investor relying on Home Insurance for Rental Income, the most devastating event is not the initial damage, but the loss of income while repairs are made.

If a burst pipe takes your property offline for four months, your commercial-grade policy’s Loss of Income Coverage steps in to replace the average revenue you would have earned from bookings, ensuring your mortgage and expenses are covered. Platform protection rarely covers this.

5. Actionable Steps to Protect Your Rental Business

- Stop Assuming: Do not assume your current HO-3 covers you. Call your agent today and explicitly state: “I am renting my property on a short-term basis via Airbnb.” If they tell you, “We can’t cover that,” you know your policy is void and you must switch.

- Compare Costs: Get quotes for both a DP-3 with a rider and a specialized commercial policy. The cost difference might be marginal, but the coverage difference is enormous.

- Review Local Ordinances: Insurance is only half the battle. Many US municipalities (like New York, San Francisco, or Austin) have strict regulations, permits, and zoning laws for short-term rentals. Operating illegally can void any insurance policy.

- Consult your local city or county government website for zoning and permitting requirements before listing your property.

- Maximize Liability: Given the high risk of US litigation, ensure your liability limit is high (at least $500,000 to $1 million). If you have a separate Personal Umbrella Policy, confirm with the underwriter that it extends coverage to the rental activity (most standard umbrella policies exclude business activity).

Secure Your Rental Revenue Today

Renting your home on platforms like Airbnb is a legitimate and lucrative business. However, running a business with personal insurance is like running a marathon in flip-flops—you are guaranteed to fail.

The Airbnb Insurance US landscape is complex, requiring a transition from personal homeowner’s coverage to a specialized policy. By acknowledging the Commercial Activity Exclusion and filling the Host Protection Insurance Gap with robust liability and loss-of-income coverage, you can enjoy the revenue of short-term rentals with true peace of mind.

Do you rely on rental income from your property? Don’t wait for a claim denial. Contact a specialized vacation rental insurance broker today to get a quote tailored to the frequency of your bookings!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.