The Essential Safety Net: Why Teachers Need Paycheck Protection

Did you know that one in four American workers will experience a disabling injury or illness that keeps them out of work for a year or more? As a dedicated educator, you pour your time and heart into the classroom, but a sudden illness—like an unexpected surgery, severe back injury, or even a lengthy stress-related leave—can stop your paycheck cold.

Disability insurance for teachers is essentially paycheck protection. It provides a monthly benefit to replace a portion of your income if you become too sick or injured to perform your teaching duties. For US teachers, navigating this market is crucial because school-provided benefits often have significant gaps. This comprehensive guide will break down the options to help you secure the best Disability Insurance for Teachers in the USA.

1. Group vs. Individual: Understanding Your Coverage Gaps

Most teachers receive some level of disability coverage through their school district or state retirement system. This is your Group Coverage. While better than nothing, it often falls short.

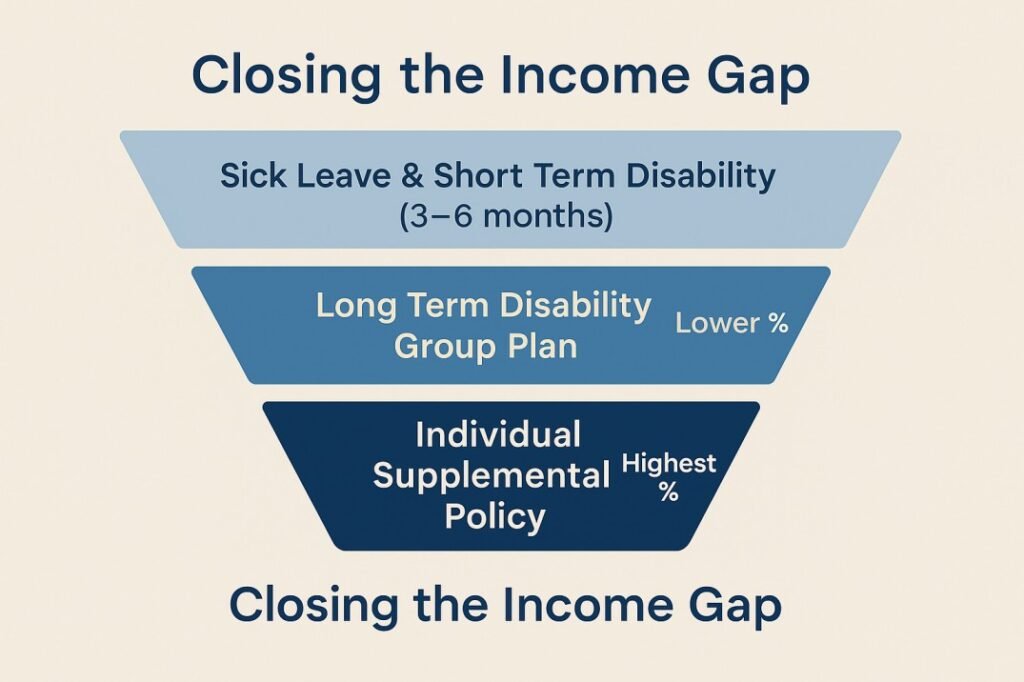

Group Short Term Disability (STD) and Long Term Disability (LTD)

Your employer-sponsored plan is typically cheaper but less flexible.

- Short Term Disability (STD) Insurance: This pays a percentage of your salary (often 60%-80%) for a short period, typically 3 to 6 months, after a brief Elimination Period (waiting period), which is usually 7 to 30 days. It helps cover the gap before a long-term policy kicks in or your sick leave runs out.

- Long Term Disability (LTD) Insurance: This takes over when the STD benefit is exhausted. It can pay benefits for many years, sometimes up to age 65 or 67. Crucially, many school-provided LTD plans may only cover 40% to 60% of your base salary, leaving a substantial shortfall.

The Power of Individual (Supplemental) Disability Insurance

An individual policy is purchased directly by you and is portable, meaning you take it with you if you change districts. It is vital for two reasons:

- Supplementation: It can boost your total benefit closer to 70% of your full income.

- Superior Definition of Disability: It often offers the gold standard of coverage, the “True Own Occupation” definition.

2. The Non-Negotiable Feature: “True Own Occupation”

This is the single most important detail to understand when buying disability coverage, especially as an educator.

- “Any Occupation” (Common in Group Plans): After the first two years, this policy defines “disabled” as being unable to work in any job for which you are reasonably qualified by education, training, or experience.

- Example: If a high school shop teacher loses the use of one hand and can no longer work a table saw (their “own occupation”), a claims adjuster might argue they could still work as a school librarian or an administrator (an “any occupation”). If they take the librarian job, their benefits are cut or eliminated.

- “True Own Occupation” (The Gold Standard): This policy considers you disabled if you cannot perform the main duties of your specific job (e.g., teaching 5th grade English). You can still receive full benefits even if you choose to work in another profession or take a different job for income. This is critical for protecting the specialty of your career.

3. Key Riders and Policy Features for Educators

Beyond the “Own Occupation” clause, look for these features:

| Feature | Why it Matters for a Teacher |

| Partial/Residual Rider | Allows you to receive a benefit if a partial disability only allows you to teach part-time or with reduced duties. |

| Future Purchase Option | Lets you increase your coverage as your salary grows without having to go through a new medical exam. |

| Cost of Living Adjustment (COLA) Rider | Increases your monthly benefit to keep pace with inflation after you’ve been on a claim for a year or more. |

| Student Loan Rider | A unique feature that provides extra funds to cover your student loan payments while you are disabled. |

Case Study: The New Teacher vs. The Veteran

- Scenario A: The New Teacher (Texas, Age 28): A newly hired elementary school teacher in Houston has only 12 accrued sick days and a group LTD policy covering only 50% of her base salary. She breaks her leg badly in an off-campus accident.

- Action: She files a claim against her Short Term Disability for 3 months. When that runs out, her Supplemental Individual LTD policy kicks in, providing a combined benefit that replaces 70% of her full salary. The True Own Occupation clause ensures her benefit is paid out even if she could technically do remote data entry.

- Key Takeaway: Her small supplemental policy saved her from quickly draining her savings during her crucial recovery period.

To help you compare different policies and understand the fine print, the National Association of Insurance Commissioners (NAIC) offers impartial consumer guides on buying individual disability insurance.

4. Financial Logistics: Taxes and Trusted Carriers

Will I Pay Taxes on My Benefits?

The taxability of your benefits is simple but often misunderstood:

- If you pay the premiums with after-tax dollars (as is typical for an individual supplemental policy), the monthly benefits you receive are tax-free.

- If your employer pays the premiums (as is typical for group plans), the monthly benefits you receive are generally taxable income.

This is yet another reason to prioritize a personally-funded supplemental plan. For official guidance on disability benefit tax rules, consult the Internal Revenue Service (IRS) Publication 525 on Taxable and Nontaxable Income.

Reputable Individual Carriers for Teachers

While major group carriers like MetLife and Unum service many school systems, highly-rated individual carriers known for their strong ‘own occupation’ policies include:

- Guardian/Berkshire

- Principal

- MassMutual

- Ameritas

- Standard (often highly rated for educators)

FAQ: Disability Insurance for Teachers

Q: Do my teacher’s sick days count as the waiting period?

A: Yes, typically. The elimination period (the waiting time before benefits begin) is often structured to run concurrently with your accumulated sick leave. This is why a shorter elimination period (e.g., 60 or 90 days) can be beneficial.

Q: Is disability insurance expensive for educators?

A: Premiums usually cost 1% to 3% of your annual salary. Since teachers are considered lower-risk than most high-skill trades, rates are generally favorable. Having an advanced degree (Master’s or PhD) can often qualify you for a discount.

Q: Does it cover pregnancy and maternity leave?

A: Yes, short term disability policies generally cover the recovery period following childbirth (typically 6-8 weeks) as a temporary disability. However, it does not cover time spent before the birth or the time for parental bonding unless medically required.

Q: What about Social Security Disability Insurance (SSDI)?

A: SSDI is a federal program that provides benefits if you are severely disabled and cannot do any substantial work for a year or more. It has a high denial rate and a long waiting period. It should only be considered a last resort, not a primary income replacement plan. You can learn more about eligibility from the Social Security Administration.

Final Word: Secure Your Greatest Asset

Your ability to earn an income is your greatest financial asset. As a teacher, your voice, your ability to manage a classroom, and your health are integral to your career. Don’t rely solely on a group policy designed for the masses.

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.