Car Insurance Plans for Students often feel like a massive financial hurdle. As an Australian student, you’re juggling HECS-HELP debts, part-time work, and the ever-increasing cost of living—the last thing you need is an overpriced insurance premium. Unfortunately, because most students fall into the “under-25” age bracket, they are statistically considered higher risk and are charged some of the steepest premiums on the market.

However, getting Cheapest Car Insurance is not impossible. It simply requires smart shopping and strategic policy choices. This comprehensive guide is designed specifically for students and young drivers across Australia, breaking down the essential cover types, revealing the best cost-saving hacks, and helping you secure affordable Insurance Plans for Students in Australia.

1. Why Car Insurance is Expensive for Australian Students

Before diving into savings, it’s vital to understand the primary factor driving up your premium: age and experience.

Insurers in Australia use data to calculate risk. Statistically, drivers under the age of 25 are involved in a disproportionately high number of road accidents. For example, young drivers (17–25) account for roughly one-quarter of all Australian road fatalities, despite making up only 10–15% of licensed drivers.

Insurers mitigate this higher risk by charging higher premiums and often applying additional excesses.

The Young Driver ‘Double Whammy’

When a young driver (usually under 25) is driving at the time of an accident, your policy is often subject to two layers of excess:

- The Basic Excess: The standard fee everyone pays when making a claim.

- The Age/Inexperienced Driver Excess: An additional excess applied because the driver at the time of the claim was under a certain age (often 25) or held their license for less than two years (e.g., a P-plater).

This combined excess can sometimes run into thousands of dollars, making minor claims impractical and reinforcing why choosing the right policy is crucial.

2. Choosing the Right Level of Cover: The Student Budget Breakdown

The biggest decision in securing affordable Car Insurance Plans is choosing the correct level of coverage for your needs. Students often drive older, lower-value cars, which makes the most expensive Comprehensive policy unnecessary for many.

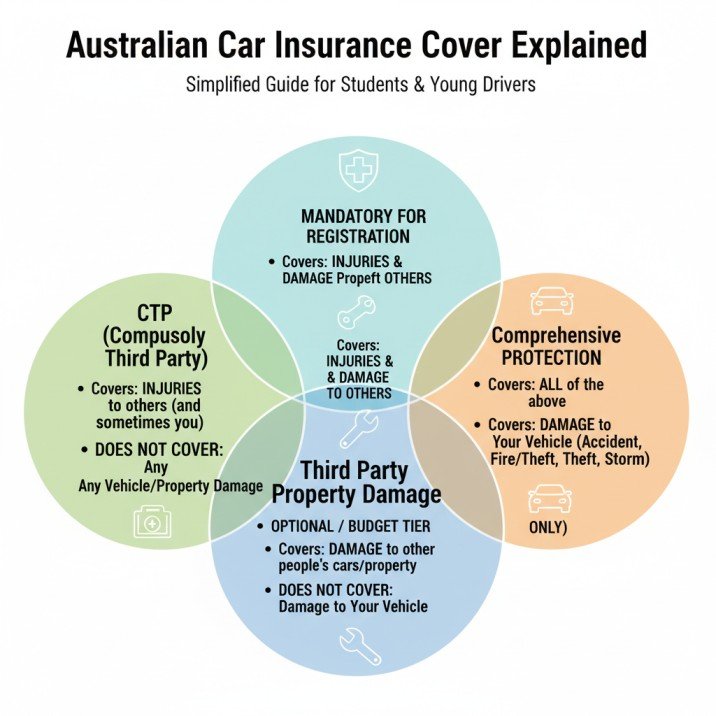

In Australia, there are four main types of Car Insurance Plans:

A. Compulsory Third Party (CTP) Insurance (Mandatory)

This is the only legally mandated car insurance in Australia. You cannot register a vehicle without it.

- What it Covers: Personal injuries or death caused to other people (and sometimes yourself, depending on the state) in an accident.

- What it DOES NOT Cover: Absolutely no damage to cars or property, including your own vehicle, the other party’s vehicle, or a fence you might hit.

- Cost & Purchase: In most states (VIC, TAS, SA, WA, NT, ACT), it is bundled into your annual vehicle registration fee. In NSW and QLD, you must choose and purchase your CTP policy separately before registration (in NSW, it’s called a Green Slip).

- Suitability for Students: This is mandatory, but not enough to protect you financially. If you are at fault in an accident, CTP will cover the victim’s medical bills, but you are personally liable for the thousands of dollars required to fix their car.

B. Third Party Property Damage (TPPD)

This is the cheapest form of optional insurance and is the entry point for financial safety.

- What it Covers: Damage you cause to other people’s cars or property (up to a limit, often $20 million).

- What it DOES NOT Cover: Any damage to your own vehicle, even if it’s a total write-off.

- Suitability for Students: Best for students driving a low-value car. If your car is worth less than $5,000, you might decide that paying for repairs yourself is cheaper than the high annual premium for Comprehensive cover. TPPD is essential for protecting you from massive out-of-pocket costs if you total a more expensive vehicle (like an expensive SUV or sports car).

C. Third Party Fire and Theft (TPFT)

This is a step up from TPPD, offering a small amount of protection for your own vehicle.

- What it Covers: All of the above (damage to other people’s property) PLUS cover for your own car if it is stolen or damaged by fire.

- What it DOES NOT Cover: Damage to your own car from an at-fault accident (e.g., if you run into a pole).

- Suitability for Students: A strong option for students who park their car on the street overnight or live in areas with higher crime rates. It gives peace of mind against theft or fire damage without the high cost of Comprehensive cover.

D. Comprehensive Car Insurance

This offers the maximum level of financial protection.

- What it Covers: All the above PLUS damage to your own vehicle (whether it’s an at-fault accident, storm damage, flood, or vandalism).

- What it DOES NOT Cover: Standard wear and tear, mechanical failures, or illegal activity (e.g., drink driving).

- Suitability for Students: Only worth the expense if your car is relatively new or worth more than $10,000 to $15,000. If you have a car loan or could not afford to replace your car if it were written off, this policy is necessary. The higher premiums for students, however, mean you should explore every discount available to make it affordable.

3. Top 7 Ways to Get the Cheapest Car Insurance Plans for Students

As a student, you are starting with a statistically high base premium, but there are powerful strategies you can use to significantly reduce your cost.

1. Increase Your Excess

This is the most immediate way to drop your upfront premium. The excess is the amount you pay out-of-pocket when you make a claim.

- How it Works: By choosing a higher basic excess (e.g., increasing it from $600 to $1,000), you signal to the insurer that you are taking on more risk. In exchange, they lower your annual or monthly premium.

- Student Strategy: Choose an excess amount you can realistically afford to pay tomorrow. If you can’t cover a $1,500 excess in an emergency, don’t select it, even if the premium looks appealing. Remember, you must also factor in the extra young driver excess (often $400 to $800) that will be added if you are under 25 and make a claim.

2. Drive Less: Explore Low-Kilometre Discounts

If you mainly use your car for commuting to university, a part-time job nearby, or just for weekend trips, you can benefit from driving less than the Australian average.

- Low-Kilometre Policies (Pay As You Drive): Several insurers offer policies specifically for low-mileage drivers (e.g., under 15,000 km per year, or even as low as 10,000 km). You can receive a discount because the less you drive, the lower the insurer’s risk.

- Telematics (Good Driver Discounts): Some newer Car Insurance Plans use telematics (small devices or smartphone apps) to track and reward safe driving behaviour. While this may not be labelled a “student discount,” it rewards the safe, responsible driver, which can be a huge benefit for a cost-conscious student.

3. Change the Primary Driver (If Applicable)

If you drive a family car but are not the person who drives it most often, ensure your policy accurately reflects this.

- The Main Driver Rule: The person who drives the car most often must be listed as the primary driver.

- Staying on a Parent’s Policy: If you live at home and occasionally drive your parent’s car (and they drive it more than you do), it is often cheaper to be listed as an additional driver on their Comprehensive policy. While this will increase their premium, the increase will likely be less than the cost of a separate Comprehensive policy for you. Warning: If you own the car or drive it every day, listing a parent as the main driver to save money is considered “non-disclosure” and can lead to a rejected claim (insurance fraud).

4. Pay Annually, Not Monthly

This is a simple, no-effort saving hack that applies across most Australian insurers.

- The Cost of Convenience: Insurers often charge a small administrative fee or interest for the convenience of paying in monthly instalments. Over a year, these fees can add up to the equivalent of an extra month’s payment.

- Student Strategy: If you can save enough to pay the full premium upfront, you will save money. If the annual premium is $1,500, paying it upfront can save you $100–$200 compared to paying monthly.

5. Choose a Low-Risk Car Model

The type of car you drive is one of the biggest determinants of your premium.

- What Insurers Look For:

- Low Market Value: Cheaper to replace if written off.

- High Safety Rating: Lower risk of serious injury (and thus lower risk for CTP claims).

- Low Repair Costs: Common, non-modified cars (e.g., popular hatches or sedans) that are cheap to repair with readily available parts.

- Low Theft Rate: Older models that are not popular with thieves.

- What to Avoid: High-performance models (even old ones), modified vehicles, imported or rare cars, and anything with a turbo/supercharger will instantly flag you as a higher risk and dramatically increase your premium.

6. Park Securely and Safely

Tell your insurer exactly where the car is parked overnight, as this significantly affects the theft component of your premium.

- Secure Parking Discount: Parking your car in a locked garage or secured carport is much safer than leaving it on the street. Insurers often provide a discount for secured parking.

- Student Strategy: If you live on campus or rent a property, find out if you can access a secure parking spot. If you are forced to park on the street, this factor will likely make your premium more expensive.

7. Compare, Compare, Compare!

No single insurer offers the Cheapest Car Insurance for every student. Because every insurer has its own unique formula for calculating risk based on your age, postcode, and vehicle, quotes can vary by hundreds, or even over a thousand dollars.

- Use Comparison Sites: Start with comparison websites to get a quick overview of who is generally cheaper for young drivers (e.g., Canstar, CHOICE, Finder).

- Check Direct Insurers: Don’t stop there. Get quotes directly from insurers who may not be listed on comparison sites, such as Bingle or ROLLiN’, which often target the budget-conscious online market.

- Call and Negotiate: Once you have a couple of cheap quotes, call your preferred insurer and ask if they can beat the price. Many will match or slightly undercut a competitor to win your business.

4. Key Considerations for P-Platers and Young Drivers

As a P-Plater (Provisional Licence holder) in Australia, you face extra restrictions and, crucially, some special insurance rules.

Check Your Policy Against Licence Conditions

P-Plater policies often include strict conditions that must be adhered to.

- Passenger Restrictions: Some policies may have exclusions or higher excesses if a driver is carrying a large number of young passengers, particularly at night.

- Engine Capacity: P-Platers often face restrictions on driving high-powered vehicles (e.g., P-Plate laws in NSW/VIC often ban modified or high-performance cars). If you violate your licence conditions, your insurer can void your policy and reject any claim.

The Problem of the Unlisted Driver

For students driving their own car, the policy must be in your name, with you as the main driver.

A common mistake is allowing a friend (e.g., another student or P-plater) to drive your car without checking your policy.

- Unlisted Driver Excess: Most policies cover “any driver” with your permission, but they will apply a huge unlisted driver excess (often $1,000 to $2,000) on top of the basic and young driver excesses if that unlisted driver is involved in an accident.

- The Golden Rule: If you regularly let a friend or housemate drive your car, list them on the policy. The small increase in premium is cheaper than a multi-thousand dollar excess.

5. Potential Providers of Cheapest Car Insurance Plans for Students

While the cheapest insurer depends entirely on your specific profile (postcode, car model, gender, etc.), certain Australian providers are known for being competitive in the budget and online market, which is where Insurance Plans for Students in Australia are often found.

| Insurer Type | Insurers Known to be Competitive for Young Drivers/Budget | Key Strategy for Students |

| Online/Budget Brands | Bingle, Budget Direct, ROLLiN’ | These often offer great savings through their online-only discounts and focus on simplified, no-frills policies. Excellent for basic TPPD or TPFT. |

| Regional/RAC Brands | RACV (VIC), NRMA (NSW), RACQ (QLD), RACT (TAS) | While sometimes pricier for Comprehensive, they offer strong customer service and may have better bundled options or discounts for members, which can be beneficial if your family uses them. |

| Direct/Traditional | AAMI, Youi, Allianz | AAMI is known for good driver training course discounts. Youi offers more flexibility in customising policies (e.g., agreed value). Always compare all three. |

Disclaimer: This table is for illustrative purposes only. The cheapest insurer for you will only be revealed through comparison quotes based on your unique circumstances.

6. Planning for the Future: Building a Safe Driving Record

The best long-term strategy for achieving low Car Insurance Plans for Students is establishing a clean driving history.

The No-Claim Bonus (NCB)

The NCB is a discount you earn for every year you hold a policy without making an at-fault claim.

- Student Benefit: When you take out your own policy (even a basic TPPD one), you begin building your NCB. After 5 or more years of safe driving, this discount can reach a maximum level (often up to 70%), which drastically reduces the cost of Comprehensive cover later in life.

- Smart Claims: Avoid making small claims, as this will reset your NCB and likely increase your premium more than the cost of the repair itself.

The 25-Year-Old Rule

The single greatest cost drop for most drivers in Australia occurs around their 25th birthday. At this age, you typically graduate from the “high-risk” pool, and the restrictive Age Excess is usually removed.

- Action Plan: If you are nearing 25, shop around aggressively for new quotes. Use your clean NCB record (if you have one) and the removal of the Age Excess to demand a significantly lower premium.

Conclusion: Drive Smart, Save Big

As a student, balancing your desire for independence with the reality of a tight budget means choosing your Car Insurance Plans for Students wisely. You may not get a specific “student discount,” but you can use your circumstances—driving less, driving a low-value car, and having a good student mindset for research—to your advantage.

The final checklist for finding the Cheapest Car Insurance in Australia:

- Mandatory: Ensure you have Compulsory Third Party (CTP) insurance.

- Basic Protection: If your car is cheap, take out at least Third Party Property Damage to protect yourself from costly legal liability.

- Hacks: Increase your excess, pay annually, and drive a low-risk vehicle.

- Compare: Get 3–5 quotes from various online and traditional insurers to find the best deal for your specific postcode and car.

By being meticulous and strategic, you can secure the necessary coverage without sacrificing your student budget. Happy, safe, and affordable driving!

REFERENCE LINKS (Main Australian Sources)

The following links are from authoritative Australian consumer and financial guidance bodies, as requested, allowing users to verify or deepen their understanding of the content.

| Source/Organisation | Relevant Resource URL |

| MoneySmart (ASIC) | https://moneysmart.gov.au/car-insurance/choosing-car-insurance (General guide on types of insurance and choosing cover.) |

| CHOICE (Consumer Advocacy) | https://www.choice.com.au/money/insurance/car/articles/young-driver-car-insurance (Guide specifically on best car insurance for drivers under 25.) |

| Canstar (Financial Comparison) | https://www.canstar.com.au/car-insurance/compare/car-insurance-under-25s/ (Direct comparison and breakdown for under-25 drivers.) |

| Insurance Council of Australia | https://insurancecouncil.com.au/news-hub/news-resources/ (Industry news, reports, and consumer help pages, useful for general context.) |

| Budget Direct / Bingle | [Note: While these are commercial sites, they were frequently cited in search results as being budget-friendly options for the target audience. |

IMPORTANT LEGAL DISCLAIMER

This article provides general information only and is not personal financial advice.

The information presented in this blog post, including all comparisons, savings tips, and policy details, is intended for informational and educational purposes only. It has been prepared without taking into account your individual objectives, financial situation, or needs.

Before making any decision about car insurance, including selecting a provider, changing a policy, or choosing an excess amount, you should:

- Consider the appropriateness of the information provided in this blog post, having regard to your own personal objectives, financial situation, and needs.

- Read the relevant Product Disclosure Statement (PDS) and Target Market Determination (TMD) from the insurer. These documents outline the terms, conditions, benefits, limitations, and exclusions of the specific insurance product.

- Seek professional advice from a qualified and licensed financial adviser or insurance broker if you require personalized recommendations.

The author and publisher disclaim all liability for any loss or damage of any kind arising from the use of, or reliance on, the information contained in this blog post. Insurance quotes and policies change frequently, and figures mentioned are indicative only.

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.