Don’t Lose Your Deposit: The Crucial First Steps to a Successful Claim

The decision to cancel a highly anticipated trip is difficult enough. The last thing you need is the stress of navigating a complex insurance claim process, fearing you’ll lose hundreds or thousands of dollars in non-refundable costs.

Fortunately, travel insurance exists to mitigate this financial risk. However, simply having the policy isn’t enough; you must execute the claims procedure precisely. A successful payout hinges on two key factors: a covered reason and meticulous documentation.

This comprehensive guide walks you through every essential stage of Filing a Claim for Trip Cancellation, ensuring you follow the correct travel insurance claim procedure from the moment you decide to cancel until the funds are back in your bank account.

1. The Golden Rule: Is Your Reason Covered?

Before you initiate Filing a Claim for Trip Cancellation, you must verify that your reason for canceling aligns with the terms of your policy. This is the single biggest factor determining claim approval or denial.

Covered Reasons vs. Exclusions

Standard trip cancellation coverage only applies when the cancellation is due to an event listed specifically in your policy—a “covered reason.”

- Common Covered Reasons:

- Sudden Illness or Injury: You, a traveling companion, or an immediate family member unexpectedly falls ill or suffers an injury requiring cancellation. (Medical records are mandatory.)

- Death: The death of you, a traveling companion, or an immediate family member.

- Severe Weather/Natural Disaster: If the destination is uninhabitable or the common carrier (airline, cruise line) ceases service for a specified time due to a named natural disaster (provided the storm wasn’t named before you bought the policy).

- Jury Duty/Subpoena: You are called to serve and cannot postpone.

- Involuntary Job Loss: You or a traveling companion are laid off from permanent employment (after purchasing the policy).

- Terrorism: A terrorist event occurs near a major city on your itinerary (subject to very strict geographical and time parameters).

- Common Exclusions (Not Covered):

- “A Change of Heart”: Simply deciding you don’t want to go or are worried about general travel advisories (unless you purchased CFAR).

- Foreseeable Events: A known issue (like a doctor-advised, pre-existing condition, or a strike announced before purchase) that was not disclosed or covered by a waiver.

- General Fear of Travel: Anxiety or non-specific concerns about local politics or general illness risk.

Review your policy purchase decision with our Understanding What Travel Insurance Covers: A Full Breakdown.

The CFAR Exception

If you purchased Cancel For Any Reason (CFAR) coverage, the rules change. CFAR allows you to cancel for any reason not specifically excluded by the policy, but it usually only reimburses 50% to 75% of your non-refundable costs. Note that CFAR must typically be purchased very early in the booking process (e.g., within 10-21 days of the initial deposit).

2. Your Claim Timeline: The Crucial Steps of the Process

Knowing how to file a trip cancellation claim involves more than just filling out a form—it’s a timed process that requires immediate action.

Step 1: Notify the Travel Suppliers Immediately (The 72-Hour Rule)

As soon as you determine your trip must be cancelled, do not delay.

- Cancel Your Bookings: Immediately contact the airline, hotel, tour operator, and any prepaid service providers.

- Request Documentation: Get written confirmation of the cancellation and detailed statements showing the non-refundable amounts you forfeited. The insurer needs proof that the travel provider did not refund you.

Step 2: Contact Your Travel Insurance Provider

Notify your insurer as soon as reasonably possible after the event that caused the cancellation.

- Call the Claims Hotline: Most insurers offer a 24/7 hotline. Call them to report the incident and obtain a claim number.

- Ask for the Required Documentation List: The agent will provide the exact forms and supporting documents needed for your specific situation. This is your essential checklist for the trip cancellation claim process.

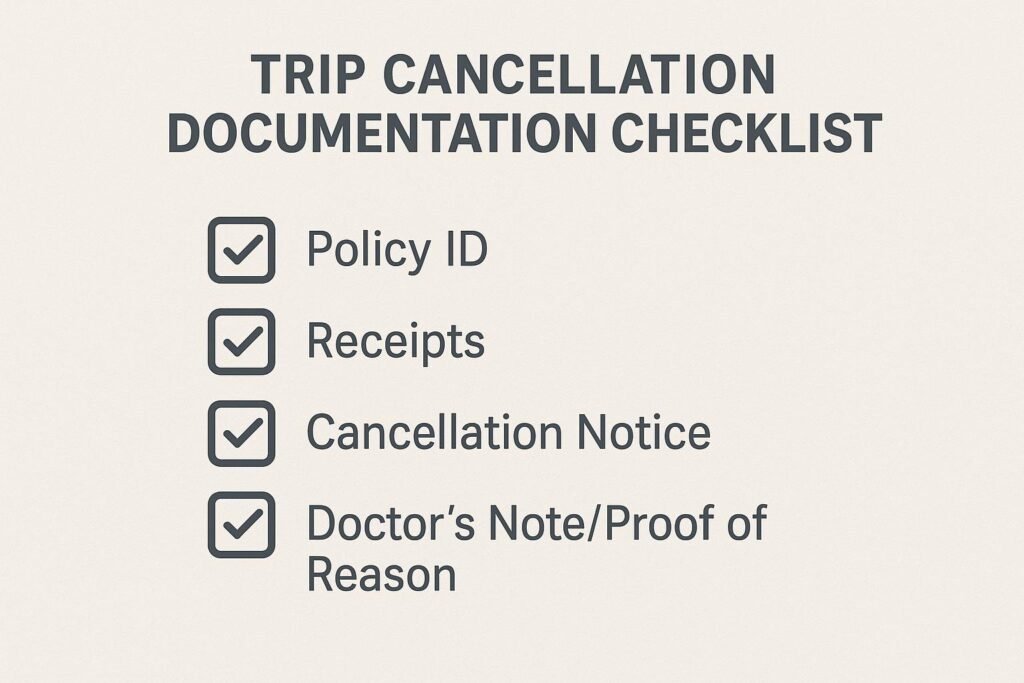

Step 3: Collect and Organize All Claim Requirements

This step is where most claims succeed or fail. Your documents must paint a clear, verifiable picture of your loss.

| Document Category | Purpose | Example Documents Required |

| Proof of Policy | Verifies coverage and dates. | Policy Declaration Page, Certificate of Insurance. |

| Proof of Loss/Cost | Proves what you paid and forfeited. | Original Booking Invoices, Receipts for all prepaid, non-refundable expenses. |

| Proof of Cancellation | Verifies services were cancelled. | Cancellation letters from the airline/hotel, Refund statements showing zero or partial refund. |

| Proof of Covered Reason | Verifies the cancellation cause is eligible. | Doctor’s Note/Medical Records (for illness/injury), Death Certificate (for death), Police Report (for theft), Official HR Letter (for job loss). |

| Claim Form | The official request for reimbursement. | Completed, signed, and dated claim form (must be accurate). |

Crucial Tip: What to do when canceling a trip claim often comes down to this: Gather more documents than you think you need. Clear, legible copies prevent delays.

3. Real-World Claims: Covered vs. Denied

Understanding your coverage requires looking at typical situations faced by US travelers.

Scenario A: Covered Emergency Trip Cancellation

Sarah and her husband had a non-refundable $\$6,000$ cruise booked. Three weeks before departure, Sarah’s mother suffers a sudden, life-threatening stroke and is hospitalized.

- Action: Sarah immediately cancels the cruise and calls her insurer to start Filing a Claim for Trip Cancellation.

- Documentation: She submits the cruise line’s cancellation invoice ($6,000 forfeited), her policy details, and a signed statement from her mother’s treating physician detailing the stroke, hospitalization dates, and why the situation prevents her from traveling.

- Outcome: Approved. Sudden, life-threatening illness of an immediate family member is a standard covered reason, verified by medical records.

Scenario B: Claim Denied Trip Cancellation (Change of Mind)

David booked a non-refundable tour to a region that later saw political protests. His State Department issues a generic travel advisory, but not an official warning or ban. David cancels, feeling unsafe.

- Action: David files a claim, citing civil unrest.

- Documentation: He submits the tour cancellation receipt and the news reports/advisory.

- Outcome: Denied. General civil unrest or fear is not typically a covered reason unless the area is specifically subject to a government-issued mandatory evacuation or a terrorist incident (as defined by the policy) occurred. David needed CFAR for this scenario.

When your trip involves political or health risks, check the official U.S. Department of State Travel Advisories page to see if your destination carries a specific Level 3 or 4 warning that might trigger coverage under some policies.

4. Submitting and Following Up on Your Claim

Most major US travel insurers allow you to submit your claim package (form and all documents) easily online or via an app. This is the fastest and most trackable method.

- Submission Tip: Use PDF files for clarity. Name your files logically (e.g., “Doctor’s Note_Smith.pdf”). Double-check that all required fields on the claim form are complete.

- Wait Times: Most insurers aim to process complete, well-documented claims within 7 to 30 days. Be patient, but track your claim status using the reference number provided.

- Claim Denials: If your claim is denied, the insurer must provide a reason. If you believe the denial is in error (e.g., they missed a key document), you have the right to appeal. Submit any missing or clarifying information immediately.

External Reference Link Suggestion: If you are experiencing difficulty or suspect an unfair process, you can find consumer information and file a complaint with your state’s insurance department or the National Association of Insurance Commissioners (NAIC).

FAQ: Your Claim for Trip Cancellation

Q: When is the best time to file the claim?

A: File the claim as soon as possible after the covered event occurs and you have cancelled your non-refundable bookings. Delaying the process can sometimes jeopardize your claim, especially if there are policy time limits.

Q: How long does it take to get reimbursed?

A: Once your claim is approved and all documents are verified, reimbursement typically takes 7 to 30 days, often issued via electronic bank transfer (ACH) or check.

Q: What if I only receive a partial refund from my travel provider?

A: Your travel insurance will only cover the non-refundable amount you forfeited. If your airline refunded you $500 of a $1,000 ticket, your insurance will only cover the remaining $500 (minus any deductible, if applicable).

Q: Is it better to call the insurer or file online?

A: Always call first to report the event and receive a claim number and instructions. Then, file the complete claim package online for the fastest processing and best tracking ability.

Preparation is the Passport to Peace of Mind

Filing a Claim for Trip Cancellation doesn’t have to be a battle. By understanding the core rule (covered reason) and proactively collecting the necessary documentation at the time of cancellation, you significantly increase your chances of a quick and successful reimbursement. The time you spend preparing your claim is an investment that protects your valuable travel dollars.

Protect your next adventure. Review your travel insurance policy’s “covered reasons” before booking your next trip to ensure you have the right protection when you need it most!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.