The Freelancer’s Dilemma: Securing Your Health Beyond the NHS

As a freelancer in the UK, you enjoy unparalleled freedom and flexibility. But with that independence comes the responsibility of managing your own safety nets – and healthcare is arguably the most crucial. While the NHS provides incredible care, many self-employed individuals find themselves facing longer waiting lists for specialist appointments, non-urgent treatments, or simply desire more control over their healthcare journey. This is where Health Insurance for Freelancers becomes an invaluable asset.

Navigating the landscape of private health insurance while also understanding the role of the NHS can feel daunting. This comprehensive guide is designed specifically for you, the UK’s independent workforce, to demystify Health Insurance for Freelancers and help you find genuinely affordable health insurance for freelancers UK.

1. Bridging the Gap: How Private Health Insurance Complements the NHS

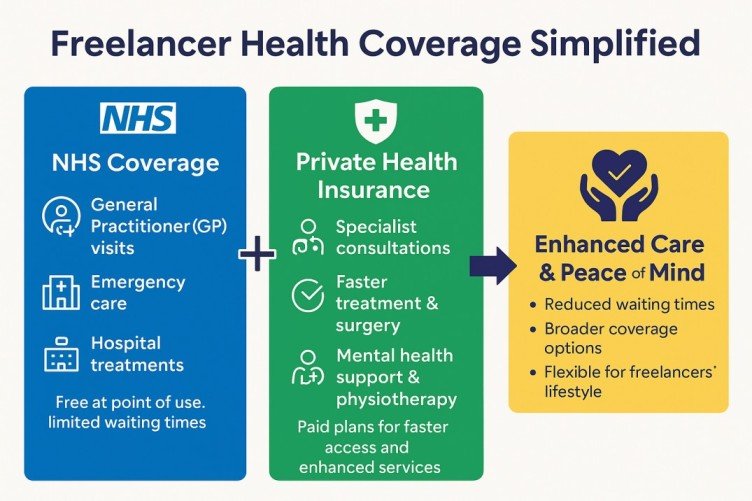

It’s a common misconception that private health insurance replaces the NHS. In the UK, it largely works in tandem. The NHS remains your go-to for emergencies, GP visits, and chronic conditions. Private health insurance steps in to offer benefits like:

- Faster Access to Specialists: Avoid lengthy waiting lists for consultations and diagnostics.

- Choice of Consultants: Select your preferred specialist and even hospital location.

- Private Hospital Rooms: Enjoy greater comfort and privacy during treatment.

- Access to Treatments Not Routinely Available on the NHS: Though less common, some innovative drugs or therapies might be available privately first.

For many, the peace of mind that comes with knowing they can access faster, more convenient care without impacting their freelance income is the primary driver for seeking self-employed health insurance UK.

Understanding “Excess” (Not “Deductible” in the UK!)

In the UK, what Americans call a “deductible” is known as an “excess.” This is the amount you agree to pay towards a claim yourself before your insurer pays the rest. Choosing a higher excess can significantly lower your monthly premiums, making low-cost health insurance for freelancers more attainable.

2. Finding Affordable Health Insurance for Freelancers UK: Key Strategies

The term “affordable” is relative, but there are concrete steps you can take to manage costs without compromising essential coverage.

a) Tailor Your Policy: Don’t Pay for What You Don’t Need

Many insurers offer flexible plans. Think about what’s most important to you:

- In-patient vs. Out-patient: In-patient care (overnight hospital stays) is typically more expensive to insure. Some policies allow you to reduce or remove out-patient cover (consultations, diagnostics without an overnight stay) to lower premiums, relying on the NHS for these.

- Hospital List: Choosing a more restricted “hospital list” (e.g., excluding central London hospitals) can make your freelancer health coverage UK more affordable.

- No Claims Discount: Similar to car insurance, a “no claims discount” can significantly reduce your premium over time if you don’t make claims.

b) Compare the Market & Specialist Brokers

Don’t settle for the first quote. Utilise comparison websites and consider speaking to a specialist health insurance broker. They understand the nuances of UK insurance for independent workers and can often find deals you might miss.

- Example: Imagine Sarah, a freelance graphic designer in Bristol, initially thought private health insurance was out of her budget. After speaking to a broker, she found a plan with a £500 excess and a restricted hospital list that covered faster access to dermatologists (her main concern) for just £35 a month – a significant saving compared to standard plans.

c) Consider Health Cash Plans (for Lower-Cost Options)

If a full private medical insurance policy is too expensive, a health cash plan could be a valuable alternative. These aren’t health insurance, but they reimburse you for everyday healthcare costs like dental check-ups, eye tests, physiotherapy, and even some GP fees, up to a set annual limit. While they don’t cover major medical treatments, they are a form of low-cost health insurance for freelancers that can help manage routine out-of-pocket expenses.

Explore our guide to Affordable Life Insurances for Teachers in the UK.

3. What to Look For: Essential Features of Private Health Insurance for Freelancers

When evaluating different policies for your freelance medical coverage, keep these key features in mind:

- Underwriting Type:

- Full Medical Underwriting: You provide your full medical history upfront. This can lead to more tailored exclusions but often a clearer understanding of what’s covered from the start.

- Moratorium Underwriting: Pre-existing conditions are automatically excluded for a period (e.g., two years), but might become covered if you don’t experience symptoms or require treatment during that time. Often simpler to set up initially.

- Chronic Conditions: Be aware that private health insurance generally excludes chronic conditions (long-term, incurable conditions like diabetes or asthma) which remain under the NHS.

- Mental Health Cover: Check if mental health consultations and treatment are included, as this is becoming an increasingly important aspect of Health Insurance for Freelancers.

For independent and free advice on choosing the right financial products, including health insurance, visit MoneyHelper (formerly Money Advice Service), a UK government-backed service.

FAQ: Health Insurance for Freelancers in the UK

Q: Does having private health insurance mean I can’t use the NHS? A: Absolutely not! Private Health Insurance for Freelancers in the UK is designed to work alongside the NHS. You’ll always have access to NHS services, especially for emergencies, your GP, and any chronic conditions.

Q: Can I get cover for pre-existing medical conditions? A: It’s challenging. Most private policies will exclude pre-existing conditions, especially in the initial years (under moratorium underwriting). Some specialised policies or older plans might offer limited cover, but this often comes at a much higher premium.

Q: How much does health insurance typically cost for a freelancer in the UK? A: Costs vary widely based on age, location, chosen excess, level of cover, and medical history. You could find basic plans starting from £20-£30 per month, rising to £100+ for comprehensive cover with a low excess.

Q: Is private medical insurance tax-deductible for freelancers? A: Generally, no. For most self-employed individuals, private health insurance premiums are not considered a tax-deductible business expense by HMRC. It’s usually paid with after-tax income.

Q: What about dental or optical care? A: Basic health insurance policies typically do not include routine dental or optical care. These are usually covered by separate health cash plans or specialist dental/optical insurance policies.

Empower Your Freelance Journey with Smart Health Coverage

Being a freelancer in the UK offers incredible rewards, but neglecting your health coverage can create significant vulnerabilities. From accessing faster specialist care to gaining more control over your medical journey, Health Insurance for Freelancers is a critical investment in your future and your ability to work.

By understanding how private health insurance complements the NHS, exploring tailored policies, and knowing what key features to look for, you can find genuinely affordable health insurance for freelancers UK that provides true peace of mind.

Empower your freelance career by securing appropriate health coverage today. Prioritise your wellbeing – your business depends on it!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.