The Hard Truth: Flooding is Not Covered by Standard US Home Insurance

If you are buying property in the United States, particularly if you are an international buyer accustomed to more comprehensive home policies, you must internalize one of the most significant differences in the US insurance market: Your standard homeowner’s insurance policy (HO-3) does not cover flood damage.

This is not an oversight or a mistake; it is a fundamental exclusion written into nearly every homeowners policy across the country.

Flooding is the most common and costly natural disaster in the US, and a few inches of water can lead to tens of thousands of dollars in repairs. If you experience a flood without separate coverage, the financial burden of rebuilding your home and replacing its contents will fall entirely on you.

This guide will explain why this gap exists, what officially counts as a “flood,” and the two critical ways you can secure the necessary coverage to ensure your investment is truly protected.

1. The Historical Reason for the Exclusion

Why do US insurers exclude flood damage when they cover other natural disasters like fire, wind, and hail? It comes down to risk assessment and catastrophe management.

A. The Definition of Unpredictable Risk

For an insurer to spread risk effectively, events need to be somewhat random and geographically distributed. Flooding does not fit this model:

- High Concentration: Floods often affect massive areas simultaneously (e.g., a major hurricane or river overflow), leading to catastrophic losses that could bankrupt a single private insurer.

- Predictability: In high-risk areas (coastal zones, flood plains), the event is not truly “unexpected.” The risk is high and often predictable, making it financially unviable for private insurers to offer affordable coverage without government assistance.

B. The Federal Intervention

Before the late 1960s, private insurers suffered astronomical losses from major floods and essentially exited the market. The federal government stepped in, recognizing the necessity of financial protection for homeowners.

In 1968, Congress passed the National Flood Insurance Act, creating the National Flood Insurance Program (NFIP), which is managed by the Federal Emergency Management Agency (FEMA). The NFIP was created to:

- Provide affordable flood insurance to property owners.

- Reduce flood damage through community floodplain management regulations.

Since 1968, the NFIP has been the primary source of flood insurance, establishing the clear separation between flood coverage and standard home insurance.

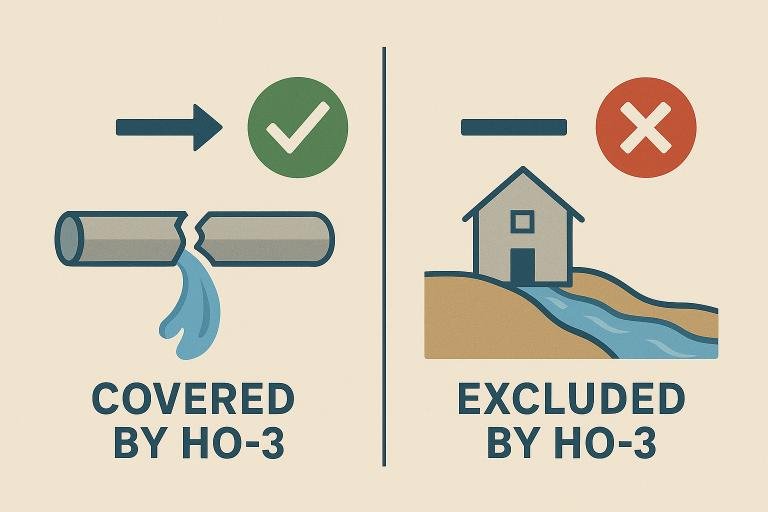

2. Water Damage vs. Flood Damage: A Crucial Distinction

The key to understanding your policy is recognizing the difference between water damage that is covered and flood damage that is excluded.

| Covered by HO-3 (Water Damage) | Excluded by HO-3 (Flood Damage) |

| Water damage that is sudden and internal to the home. | Water damage that is external and enters the home from the outside. |

| Examples: Burst pipes, accidental overflow from an appliance (toilet, washing machine), or water entry from a hole in the roof/wall caused by a windstorm. | Examples: Overflowing rivers or lakes, heavy rainfall causing surface water runoff, storm surge from an ocean or sea, or rapid accumulation of snowmelt. |

Crucial Tip: A sewer backup is often not covered by either policy unless you add a specific sewer backup endorsement to your standard HO-3 policy. However, if the sewer backup is a direct result of a major external flood event, it may be covered by your flood policy.

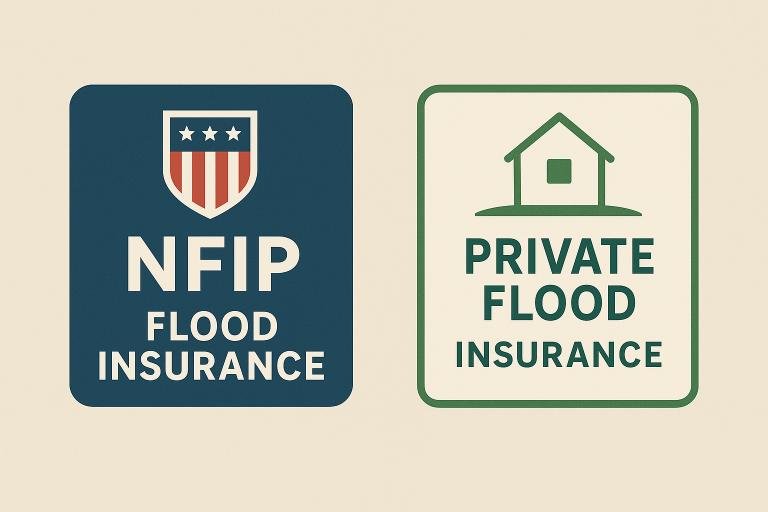

3. The National Flood Insurance Program (NFIP Explained)

The NFIP is the backbone of flood protection in the US. Policies are sold through private insurance companies (known as the Write Your Own or WYO Program) but are underwritten and backed by the federal government (FEMA).

A. Key Coverage Limits (NFIP)

The NFIP offers a standardized policy with fixed limits, which can be inadequate for high-value properties:

| Coverage Type | Maximum NFIP Limit | Coverage Scope |

| Building Property | $250,000 | Structure, foundation, plumbing, electrical, central air systems, and attached garages. |

| Personal Property (Contents) | $100,000 | Personal belongings like furniture, electronics, and clothing. |

B. Why Flood Insurance is Required USA

If your property is located in a Special Flood Hazard Area (SFHA), also known as a high-risk flood zone (Zone A or V) as designated on a FEMA Flood Insurance Rate Map (FIRM):

- Lender Requirement: Your mortgage lender (if federally regulated or insured) is legally mandated to require you to purchase flood insurance.

- Waiting Period: The NFIP typically imposes a 30-day waiting period before the policy takes effect. This prevents people from buying insurance only when a hurricane or storm is imminent. The waiting period is waived only in specific circumstances, such as when coverage is required for a new mortgage closing.

To check your property’s official flood risk status and view FEMA Flood Maps, you can consult the official FEMA Flood Map Service Center.

4. The Rise of Private Flood Insurance

The NFIP limits ($250,000/$100,000) are often too low for modern, high-value homes, especially in expensive coastal or metropolitan areas. This inadequacy, coupled with advances in risk modeling, has led to a growing market for Private Flood Insurance.

NFIP vs. Private Flood Insurance: Key Differences

| Feature | NFIP (Federal Program) | Private Flood Insurance (Market) |

| Maximum Limits | $250,000 Dwelling / $100,000 Contents | Often up to $1 Million or more for dwelling and contents. |

| Loss of Use (ALE) | Excluded | Often Included (pays for temporary living expenses if you’re displaced). |

| Basement Coverage | Limited to structure, appliances; Excludes finished walls/flooring, personal items. | More comprehensive for finished basements and personal property. |

| Waiting Period | 30 days | Often 7–14 days or less, depending on the carrier and state. |

| Cost | Standardized, risk-based pricing (FEMA’s Risk Rating 2.0). | Can be more competitive than NFIP in some areas, or provide higher limits at comparable cost. |

| Lender Acceptance | Universally accepted by federally regulated lenders. | Widely accepted by most federally regulated lenders as an alternative to NFIP. |

5. Actionable Steps for Home Buyers (Especially International)

If you are purchasing a US home, especially as an international investor, securing the right flood protection is non-negotiable. Follow these steps carefully:

- Determine Your Flood Zone: Use the FEMA portal (link above) to check the property’s flood risk. Your mortgage lender will do this anyway, but knowing upfront is essential for budgeting and understanding requirements.

- Budget for Separate Coverage: Always assume you will need to buy flood insurance as a separate cost. It is not bundled with your standard homeowner’s premium. Factor this into your monthly or annual property expenses.

- Compare NFIP and Private Options: Don’t automatically default to the NFIP. Get quotes for both. Private Flood Insurance may offer higher limits, coverage for Additional Living Expenses (ALE) not found in the NFIP, and potentially a more competitive premium, especially if your property is mapped into a high-risk zone but sits on higher ground or has effective mitigation measures.

- Buy Early & Strategically: Do not wait until closing day. Due to the waiting period, you risk a significant gap in coverage or delaying your closing if the policy is not secured 30 days in advance (unless the waiting period is specifically waived for a mortgage closing transaction). Plan well ahead.

- Review Elevation Certificates: If your home is in a high-risk zone, an Elevation Certificate (EC) can significantly impact your flood insurance premium. It documents your home’s elevation relative to the base flood elevation. Your builder or a surveyor can provide this.

Secure Your Investment from the Ground Up

The rule is simple and absolute: standard US home insurance does not cover flood damage.

For international buyers, this Federal Gap is perhaps the most critical insurance lesson when acquiring US property. By actively seeking out either comprehensive NFIP coverage or the expanded benefits of Private Flood Insurance, you move beyond the limitations of a standard HO-3 policy and safeguard your valuable investment from one of nature’s most destructive and costly forces.

Are you closing on a US property? Don’t leave your investment vulnerable. Contact a specialized US insurance broker today to compare NFIP and Private Flood Insurance quotes and ensure your coverage is active before closing!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.