Investing in Tomorrow: Why Young Teachers Need Life Insurance Today

As a young teacher, you’re building futures every day – in your classroom, shaping young minds, and nurturing the next generation. Your days are filled with lesson plans, grading papers, and perhaps navigating your first few years of a rewarding but often financially modest career. The idea of “life insurance” might feel like something for much later in life, perhaps when you’re older, have a mortgage, or a larger family. But here’s a vital truth: Life insurance for young teachers is one of the smartest, most affordable financial decisions you can make right now.

Whether you’re just starting to pay off student loans, dreaming of buying your first home, or contemplating starting a family, life insurance provides an invaluable financial safety net. It ensures that those you care about most won’t be burdened by debt or a sudden loss of income if the unexpected happens. This guide will demystify life insurance for teachers, exploring your best options, understanding benefits, and helping you make informed choices for your financial wellbeing.

1. Beyond the Classroom: Why Life Insurance is Crucial for Young Teachers

Many young teachers might think, “I’m healthy, I don’t have dependents yet, so why do I need life insurance?” The reasons are more compelling than you might think, especially for early-career educators.

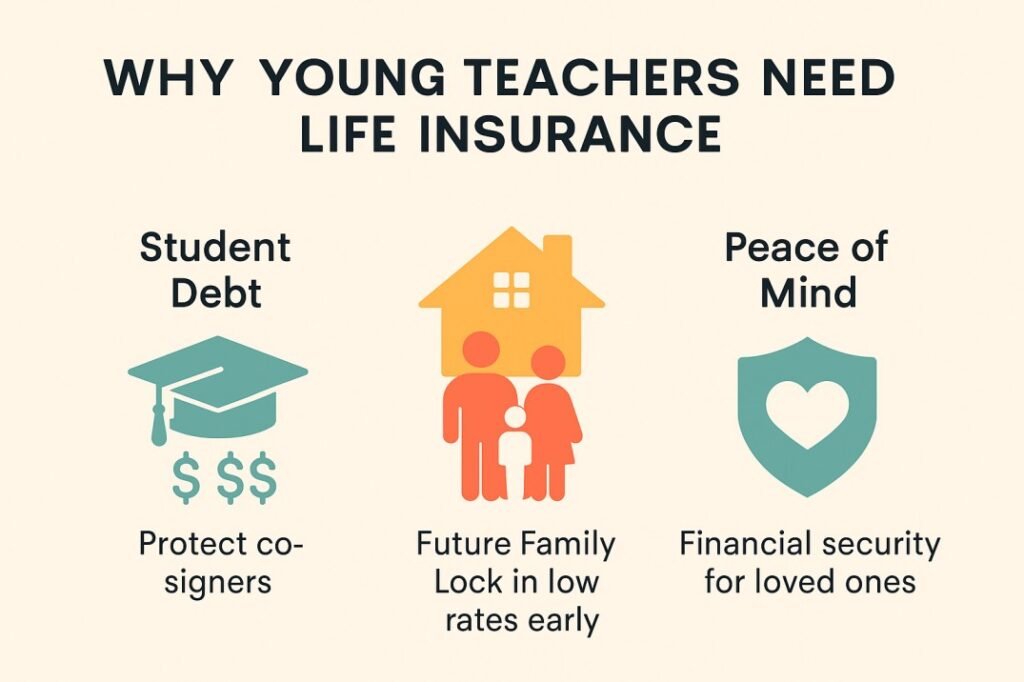

- Student Loan Debt: Many teachers graduate with significant student loan debt. If something were to happen to you, this debt could potentially fall to co-signers (like parents) or your estate, creating a huge financial burden for your loved ones.

- Future Dependents: Even if you don’t have a family now, you likely plan to. Purchasing life insurance for young teachers while you’re young and healthy means significantly lower premiums that can be locked in for decades. When you do have a spouse, children, or other dependents, that affordable policy will already be in place.

- Income Replacement: While your current salary might not be at its peak, it’s still a vital contribution. Life insurance provides a financial cushion to replace that income for your beneficiaries, allowing them to maintain their lifestyle, cover daily expenses, and achieve future goals.

- Burial and Final Expenses: Even without dependents, funeral costs can easily run into the thousands. A modest life insurance policy can cover these immediate expenses, sparing your family from an unexpected financial strain during a difficult time.

- Mortgage or Other Debts: If you co-own a home or other significant assets with a partner, life insurance can ensure they aren’t left to shoulder the entire financial responsibility alone.

Understanding these points highlights why why teachers need life insurance is a key component of sound financial planning.

Case Study: Sarah’s Student Loan Protection

Sarah, a 24-year-old first-grade teacher in Austin, TX, had $40,000 in student loan debt co-signed by her mother. While healthy, she worried about her mom’s financial strain if anything happened to her. Sarah secured a 20-year term life insurance policy for $100,000. Her monthly premium was incredibly affordable, under $20. If the unthinkable occurred, the payout would clear her student loans and provide an additional buffer for her family, preventing a significant financial burden. This demonstrates essential financial planning for teachers.

2. Choosing Your Path: Best Life Insurance Plans for Young Professionals

When exploring life insurance for young teachers, you’ll primarily encounter two main types: Term Life Insurance and Whole Life Insurance.

a) Term Life Insurance: The Affordable & Flexible Choice

For most young teachers and budget-conscious professionals, term life insurance for educators is the most recommended and popular option.

- How it Works: It provides coverage for a specific period (a “term”), typically 10, 20, or 30 years. If you pass away within that term, your beneficiaries receive a death benefit.

- Pros:

- Affordability: Term policies are significantly cheaper than whole life policies, especially when you’re young and healthy. This makes affordable life insurance for teachers a reality.

- Simplicity: Easy to understand and straightforward.

- Flexibility: You can choose a term that aligns with your financial obligations (e.g., until student loans are paid off, until children are grown, or until retirement).

- Cons:

- It only covers you for the chosen term. If you outlive the term, coverage ends unless you renew (usually at a higher rate) or purchase a new policy.

b) Whole Life Insurance: Long-Term Coverage with a Cash Value

Whole life insurance is a type of permanent life insurance.

- How it Works: It covers you for your entire life, as long as premiums are paid. It also builds “cash value” over time, which you can borrow against or surrender for cash.

- Pros:

- Lifetime Coverage: Never expires.

- Cash Value: A savings component that grows tax-deferred.

- Cons:

- Expensive: Premiums are significantly higher than term life insurance, making it less ideal for young teachers focused on immediate budget concerns.

- Complexity: Can be more complex to understand.

For most young teachers, starting with an affordable term life policy allows you to secure substantial coverage when it’s most crucial, without stretching your budget. Later, as your income grows, you can revisit permanent options if they align with your broader financial goals. These are important insurance options for new teachers to consider.

3. Determining How Much Life Insurance You Need

One of the biggest questions when considering life insurance for young teachers is “How much coverage do I actually need?” There’s no one-size-fits-all answer, but here’s a common formula:

- D.I.M.E. Method:

- Debt: Total all your debts (student loans, car loans, credit card debt, shared mortgage).

- Income: Multiply your annual income by the number of years you want to provide for your dependents (e.g., 5-10 years).

- Mortgage: The outstanding balance on your home loan.

- Education: Future education costs for children or yourself.

Add these totals together. This provides a good starting point for your coverage amount. Many young teachers might start with a policy of $100,000 to $500,000, depending on their debt and future plans.

Case Study: Mark’s Growing Family Needs

Mark, a 28-year-old middle school teacher in Seattle, WA, recently got married. They plan to have children in the next few years and have a combined $300,000 mortgage. Mark’s annual salary is $55,000. Using the D.I.M.E. method, he estimated:

- Debt: $20,000 (car loan, credit card)

- Income: $55,000 x 7 years = $385,000

- Mortgage: $300,000

- Education: $0 (for now) Mark realized he needed a policy of around $700,000 to adequately protect his wife and future children. He found a 30-year term policy for this amount, locking in low rates while he was young and healthy. This foresight is a prime example of effective financial planning for teachers.

For unbiased information and tools to estimate your life insurance needs, visit the Life Happens organization, which is committed to educating consumers about the importance of life insurance.

4. How to Find Affordable Life Insurance for Teachers

Finding the right policy doesn’t have to be complicated or expensive. Here are key strategies for securing affordable life insurance for teachers:

- Start Young and Healthy: This is the #1 factor for low premiums. The younger and healthier you are when you apply, the cheaper your rates will be.

- Compare Quotes: Don’t just go with the first offer. Work with an independent agent or use online comparison tools to get quotes from multiple providers. (For readers specifically in the UK, you can explore the best options for affordable life insurance for teachers in the UK here.)

- Consider Group Life Insurance (Employer-Provided): Many school districts offer a basic group life insurance policy as an employee benefit, often one to two times your annual salary. This is a great start, but it’s usually not enough on its own. It’s often term life and ends if you leave the job. Think of it as supplemental, not primary.

- Choose a Term Policy: As discussed, term life offers the most coverage for your dollar.

- Maintain a Healthy Lifestyle: Factors like smoking, obesity, and certain health conditions will increase your premiums.

- Work with an Independent Agent: An independent agent can shop around with multiple carriers to find the best life insurance plans for young professionals that fit your specific needs and budget.

These life insurance tips for young professionals ensure you get the most value.

To understand consumer protections and find licensed insurance providers in your state, consult your State’s Department of Insurance website. The National Association of Insurance Commissioners (NAIC) also provides a consumer information source.

FAQ: Life Insurance for Young Teachers

Q: Is group life insurance through my school enough?

A: Usually not. Group policies are a good start and often free or very low cost, but they typically offer limited coverage (1-2x your salary) and are tied to your employment. A personal policy ensures continuous, adequate coverage regardless of your job.

Q: Can I get life insurance if I have student loan debt?

A: Absolutely! Student loan debt is a key reason to get life insurance, especially if your loans are co-signed or if your family would be responsible for them. Your debt level will not prevent you from getting coverage.

Q: How long of a term should a young teacher choose?

A: Common terms are 20 or 30 years. Consider a term that covers you until major debts (like a mortgage) are paid off, or until your children are financially independent. Many teachers choose a 30-year term to lock in low rates for a significant portion of their career.

Q: What if I decide to leave teaching? Does my life insurance still apply?

A: If you have a personal policy (not just group coverage from your school), it will continue to apply regardless of your employer, as long as you pay the premiums. This flexibility is a major benefit of securing your own teacher insurance plans.

Q: Are there any special life insurance discounts for educators?

A: While specific “teacher discounts” on individual life insurance are rare, your stable profession and often healthy lifestyle can contribute to competitive rates. The best way to find affordable life insurance for teachers is to compare quotes widely while you are young and healthy.

Teach, Inspire, and Live Securely: Your Future is Protected

As a young teacher, your impact extends far beyond the classroom. Taking proactive steps to secure your financial future with life insurance for young teachers is an act of profound responsibility and love, not just for yourself, but for those who depend on you. It ensures that your legacy of care and dedication can continue, even if you can’t be there.

Don’t let perceived complexity or cost deter you. Now is the best time to secure affordable rates and build a foundation of financial peace of mind. Your future self, and your loved ones, will thank you.

Take the first step towards lasting financial security. Explore personalized life insurance quotes today and invest in your protected future!

P.S. To ensure your loved ones are fully prepared, you can also review a step-by-step guide to the life insurance claim process.

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.