From Overseas Adventure to Ouch: Why Knowing Your Expat Medical Claim Process is Crucial

The dream of living abroad is often filled with visions of exploring new cultures, advancing careers, or studying in exotic locales. What rarely makes it into that idyllic picture is the less glamorous, but critically important, reality of healthcare in a foreign land. Getting sick or having an accident overseas can be incredibly stressful, not just physically, but financially. Without a clear understanding of the Medical Insurance Claim Process for Expats, a simple doctor’s visit or an emergency trip to the hospital could lead to unexpected bills and overwhelming confusion.

Whether you’re a seasoned expat, an international student, a digital nomad, or an employer managing expat benefits, mastering your medical insurance for expats is non-negotiable. This comprehensive guide will demystify the Medical Insurance Claim Process for Expats, providing actionable steps, essential tips, and peace of mind for your global adventures.

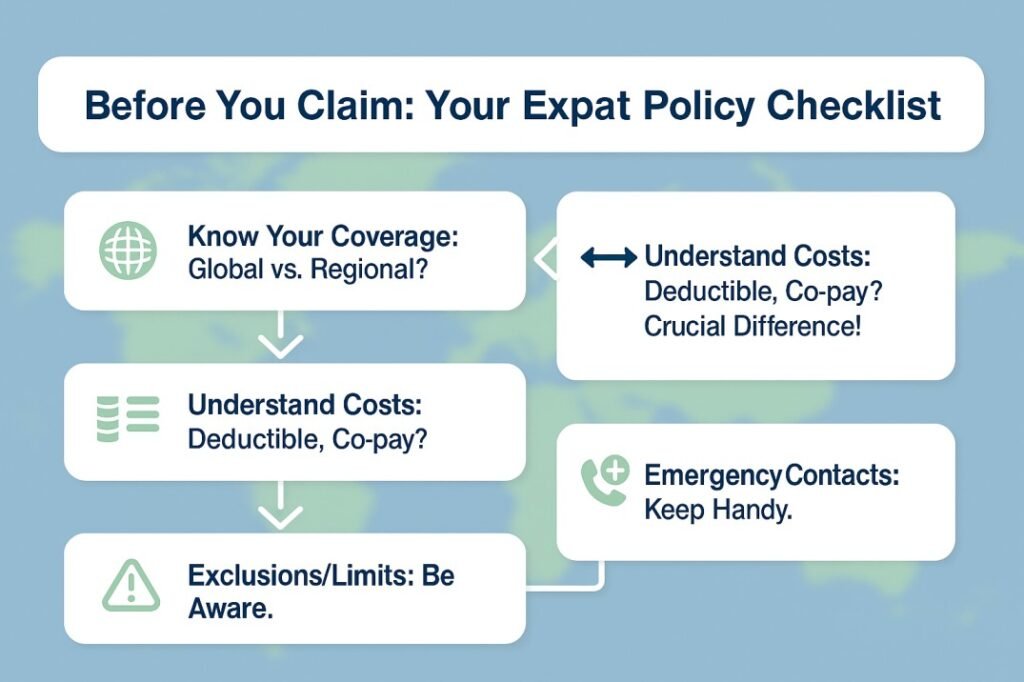

1. Understanding Your Expat Health Insurance: Know Before You Go

Before you even think about filing a claim, the most critical step is to thoroughly understand your expat health insurance policy. International health insurance differs significantly from a standard domestic plan.

Key Policy Components to Understand:

- Coverage Area: Does your policy cover you globally, or are there exclusions (e.g., your home country, specific high-risk regions)?

- Deductibles/Excess: The amount you must pay out-of-pocket before your insurance begins to cover costs.

- Co-insurance/Co-pay: Your share of the cost for a covered healthcare service after you’ve met your deductible.

- Direct Billing vs. Reimbursement: This is crucial for the claims process.

- Direct Billing (or Cashless Facility): Your insurer pays the hospital or clinic directly. This is often available for planned treatments or within a network of approved providers. It’s the ideal scenario for smooth expat insurance claim procedure.

- Reimbursement: You pay upfront, then submit a claim to your insurer for reimbursement. This is common for doctor’s visits, prescriptions, and emergencies outside preferred networks.

- Exclusions: What your policy doesn’t cover (e.g., pre-existing conditions, specific treatments, high-risk activities).

- Limits: Maximum amounts the policy will pay for specific services (e.g., annual limits, per-condition limits).

- Emergency Contact Information: Keep your insurer’s 24/7 emergency assistance number readily available.

Knowing these details upfront for your medical insurance for expats can save you significant stress and expense when a claim arises.

Case Study: A Routine Visit in Berlin

Maria, an American expat teaching English in Berlin, needed to see a doctor for a persistent cough. Her expat health insurance plan covered routine outpatient visits but required reimbursement. Before her appointment, she checked her policy’s “reimbursement” section. She paid the German doctor’s fee upfront (€80), ensuring she got a detailed, itemized receipt in English (or translated). This prepared her for the subsequent Medical Insurance Claim Process for Expats.

2. Step-by-Step: The Medical Insurance Claim Process for Expats

Navigating a foreign healthcare system and dealing with paperwork can be daunting, but following a clear process makes it manageable. This is your guide on how to file medical claims overseas.

Step 1: Seek Medical Attention (The “Incident”)

- Emergency: In a genuine emergency, prioritize getting immediate medical help. Call local emergency services. Don’t worry about insurance paperwork until you’re stable. As soon as possible, or have someone do it for you, contact your insurer’s 24/7 emergency hotline.

- Non-Emergency: For routine care, try to find a doctor or facility within your insurer’s network, if they have one, as this often facilitates direct billing.

Step 2: Gather Essential Documentation (The Paper Trail)

This is the most critical part of any health insurance claims abroad. Be meticulous!

- Itemized Bill/Invoice: This is non-negotiable. It must be detailed, showing the date of service, description of services, cost of each service, and the name/address of the medical provider. Request it in English if possible, or arrange for a certified translation if required by your insurer.

- Proof of Payment: Receipts, credit card statements, bank transfers showing you paid the medical provider.

- Medical Report/Diagnosis: A brief report from the doctor detailing your condition, diagnosis, and treatment. This helps your insurer understand the claim.

- Prescription Details: If medication was involved, a copy of the prescription and the pharmacy receipt.

- Referral Letter (if applicable): If a specialist visit required a referral from a general practitioner, include this.

- Your Policy Number: Always include this on all documentation.

Step 3: Contact Your Insurer and Submit the Claim

- Initial Notification: For emergencies, you (or someone on your behalf) should contact your insurer’s assistance line as soon as feasible. For non-emergencies, check your policy for specific notification timelines (e.g., “within 30 days of service”).

- Claim Form: Your insurer will provide a claim form (usually downloadable from their portal). Fill it out completely and accurately.

- Submission: Submit the completed form along with all gathered documentation. Most insurers offer online portals, email, or physical mail. Online portals are generally the fastest and allow you to track your international health insurance claims.

Case Study: An Emergency in Bangkok

David, a digital nomad in Bangkok, had a severe allergic reaction requiring an emergency room visit. After stabilizing, his partner called their expat insurer’s 24/7 line. The insurer initiated direct billing with the hospital. For follow-up prescriptions and a subsequent check-up, David paid upfront. He diligently collected itemized receipts and a medical report in English for everything. His clear understanding of the Expat insurance claim procedure meant a smooth reimbursement for his out-of-pocket costs.

Internal Link Suggestion: For more tips on staying healthy abroad, read our guide on [internal link to a blog post about ‘Global Healthcare Safety Tips for Travelers’].

3. Common Challenges and Solutions in Expat Medical Claims

Even with preparation, unique challenges can arise when dealing with medical insurance for expats.

- Language Barriers: Request documentation in English or ask the medical provider if they offer translation services. Many international hospitals cater to expats.

- Unfamiliar Systems: Healthcare systems vary widely. Your insurer’s assistance line can often guide you on local protocols or recommend English-speaking doctors.

- Waiting Periods: Be aware of waiting periods for certain treatments (e.g., maternity, some specialist procedures) which apply after your policy starts.

- Pre-Existing Conditions: These are a common reason for denied claims. Ensure you declared all conditions during application and understand any exclusions.

- Missing Documentation: The most frequent cause of delays. Always get itemized bills and proof of payment.

Solution: Always clarify with your insurer before undergoing expensive or planned treatments. Their assistance line is there to help confirm coverage and guide you through local processes. This proactive approach is a vital insurance tip for expats.

For general health information for US citizens living abroad and travel advisories, consult the U.S. Department of State website, specifically their “Health Abroad” section

.

4. Maximizing Your Benefits and Ensuring Smooth Processing

To make your Medical Insurance Claim Process for Expats as smooth as possible, proactive measures are key.

- Read Your Policy Document: This sounds obvious, but many don’t. It’s your contract and ultimate source of truth.

- Utilize Your Insurer’s App/Portal: Many expat insurers have user-friendly apps or online portals for submitting claims, finding network providers, and tracking progress.

- Keep a Digital Record: Scan or photograph all physical documents as soon as you receive them. Store them securely (e.g., cloud storage).

- Communicate Clearly: When contacting your insurer, provide your policy number, a concise explanation of the situation, and be ready with your documentation.

- Follow Up: If you haven’t heard back within the insurer’s stated processing time, follow up politely.

This diligence with your expat health insurance ensures you get the most out of your plan.

FAQ: Medical Insurance Claim Process for Expats

Q: How long does it typically take for an expat medical claim to be processed?

A: Processing times vary by insurer and complexity of the claim, but typically range from 5-15 business days for simple claims once all documentation is received. Complex claims or those requiring further investigation may take longer.

Q: What if I lose a receipt? Can I still claim?

A: Without an itemized bill and proof of payment, claiming can be very difficult, often impossible. Always request and keep original receipts. If lost, contact the medical provider for a duplicate and explain the situation to your insurer immediately.

Q: Do I need to translate all my medical documents?

A: Your insurer will specify. Often, a detailed, itemized bill in the local language is sufficient if key terms are understandable. However, for complex medical reports, a certified translation might be required. Always ask your insurer first.

Q: What is a “preferred provider network” for expats?

A: Many expat insurers have networks of hospitals, clinics, and doctors worldwide with whom they have direct billing agreements or negotiated rates. Using these providers can simplify the Medical Insurance Claim Process for Expats and reduce out-of-pocket costs.

Q: Can I claim for routine dental check-ups with expat medical insurance?

A: Most basic expat medical insurance plans do not cover routine dental or optical care. This often requires an additional “dental and optical” rider or a separate policy. Always check your specific plan’s benefits.

Your Global Health, Secured: Claim with Confidence

Embarking on life as an expat is an incredible journey, and understanding your healthcare protection shouldn’t add to the adventure’s anxieties. By mastering the Medical Insurance Claim Process for Expats, you empower yourself to navigate foreign medical systems with confidence, ensuring you receive the care you need without unexpected financial burdens.

From knowing your policy inside and out to meticulously documenting every visit, each step you take contributes to a smoother, stress-free experience. Equip yourself with this knowledge, and make your global living truly seamless and secure.

Ensure your peace of mind abroad. Review your expat medical insurance policy and understand your claim process today!

Written by Imran Khan

Founder & Lead Content Specialist, Claimifio

Imran Khan brings over 8 years of experience in digital content creation and web development to Claimifio. As a Senior WordPress Developer at Zikra Infotech LLC, he has worked extensively with healthcare providers including emergency rooms, medical clinics, and specialty practices – giving him deep insight into the challenges patients and families face when navigating insurance systems.

His mission with Claimifio is simple: make insurance understandable for everyone. Every guide is researched thoroughly, written in plain English, and designed to help you take action with confidence.